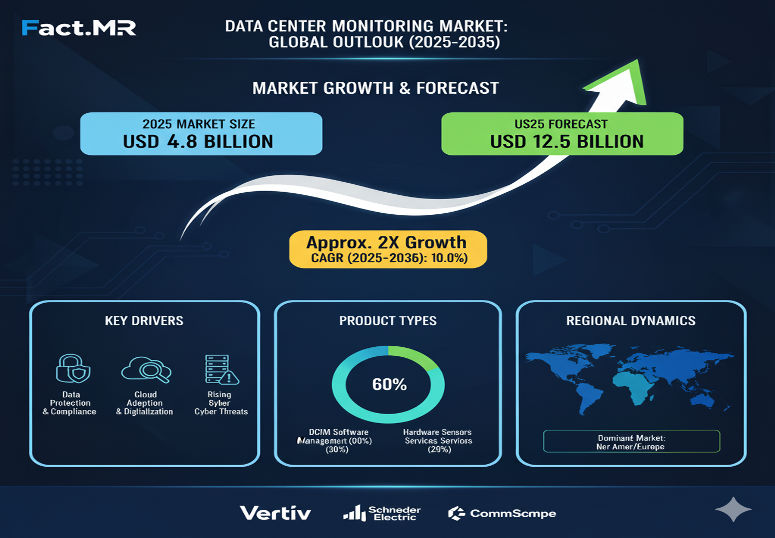

In an era of relentless data growth, cloud expansion, and edge computing proliferation, data centers are under pressure like never before. Ensuring reliability, uptime, and efficiency isn’t optional—it’s foundational. That’s fueling demand in the Data Center Monitoring Market, which enables operators to observe everything from power, temperature, and humidity to performance, security, and predictive faults. Recent analyses put the market value for 2025 at roughly USD 4.8 billion, with expectations that it will more than double to about USD 12.5 billion by 2035, growing at a compound annual growth rate (CAGR) around 10% over that period.

Core Components, Segmentation & Use Patterns

The market divides primarily by component (software, hardware, services), deployment model (cloud-based vs on-premises), and organization size (large enterprises vs small & medium enterprises, SMEs). Key observations include:

-

Software solutions dominate the component mix today, accounting for approximately 60% share in 2025. These include analytics, alerting, dashboards, and predictive tools.

-

Large enterprises are currently the biggest users of monitoring systems, accounting for around 65% of demand. These organizations have complex infrastructures, high uptime requirements, and both the budget and internal expertise to adopt and maintain advanced systems.

-

Deployment models are shifting; while on-premises monitoring remains important, especially where data sovereignty, latency or environment make that desirable, cloud-based monitoring is gaining favor for its scalability, flexibility, and lower upfront costs.

Regional Insights: United States & Europe

United States

The U.S. is expected to lead global growth in the data center monitoring market, driven by high concentration of hyperscale, cloud, and colocation data centers, large enterprise presence, and strong investment in AI-powered infrastructure monitoring. Forecasts indicate U.S. growth rates in the mid-teens CAGR over the next decade as operators invest in predictive maintenance, energy optimization, and AI/ML-enabled monitoring platforms.

Key U.S. priorities include reducing operational cost, preventing downtime, ensuring compliance with SLAs, and integrating monitoring with energy efficiency and sustainability goals.

Europe

In Europe, demand for data center monitoring is also rising steadily, particularly in Germany, UK, France, and the Nordics. European operators place a high premium on reliability, regulatory conformity (including environmental compliance and energy usage reporting), and sustainability. Monitoring solutions that deliver real-time visibility, energy metrics, and predictive warning of failures are particularly valued.

Cost pressures and regulatory oversight tend to slow deployment a bit compared to the U.S., but the premium placed on safety, privacy, and environmental impact give European adopters strong incentives for high-function solutions.

Recent Developments & Trends

Several recent shifts are reshaping the data center monitoring market in meaningful ways:

-

There’s increasing integration of AI, machine learning, and predictive analytics, enabling anomaly detection, predictive failure alerts, and optimized maintenance schedules.

-

Edge computing and hybrid/edge-cloud infrastructure growth demand monitoring systems that span distributed environments with low latency and high reliability.

-

Sustainability is becoming a core part of monitoring: system features for energy usage, cooling efficiency, power utilization effectiveness (PUE), carbon footprint are now often built in.

-

Monitoring vendors are expanding into services — managed monitoring, real-time dashboards, remote monitoring and optimization — to support institutions that lack deep internal monitoring expertise.

Key Players & Competitive Landscape

The Data Center Monitoring Market is shaped by both infrastructure and monitoring specialists. Prominent participants include:

-

Schneider Electric — strong in infrastructure monitoring and management platforms.

-

Vertiv Holdings — known for both hardware components (power, cooling monitoring) and end-to-end monitoring systems.

-

Johnson Controls — with strength in facility automation and environmental monitoring.

-

Siemens AG, Emerson Electric, ABB Ltd. — these firms bring strong hardware, industrial IoT, and automation expertise.

-

Other focused players such as Rittal GmbH, AKCP, Geist, Panduit compete especially on niche hardware, sensors, and feature depth.

Differentiation comes down to analytics sophistication, ease of integration, sensor accuracy and reliability, scalability, and cost of ownership. Vendors that can deliver strong prediction of failures, minimal false alarms, and real value in energy savings and operational cost reduction are being rewarded.

Challenges & Barriers to Adoption

Despite strong growth potential, several constraints remain:

-

Upfront costs and complexity: Deploying hardware sensors, integrating with legacy infrastructure, configuring software, and training staff remain barriers, particularly for smaller data centers or in regions with limited technical capacity.

-

Data overload and false positives: Monitoring generates massive amounts of data; filtering noise, dealing with false alarms, and deriving actionable insight without overwhelming operations teams is a real challenge.

-

Fragmented standards and integration issues: Multiple vendors, varied hardware, differing protocols and standards make integration difficult. Interoperability is a frequent concern.

-

Regulatory, privacy and security concerns: Ensuring monitoring data is secure, respecting privacy, and meeting local regulation (e.g., around data handling or environmental reporting) is essential but increases complexity and cost.

Browse Full Report: https://www.factmr.com/report/data-center-monitoring-market

Outlook & Strategic Implications

For companies in or entering this market, strategic success will likely depend on several factors:

-

Analytic intelligence — Vendors with strong AI/ML capabilities that offer actionable insights and predictive performance will dominate.

-

Scalable, hybrid monitoring platforms — Able to operate across cloud, edge, hybrid and distributed infrastructure with consistent reliability.

-

Energy & sustainability measurement — As environmental concerns become regulatory and customer demands, monitoring must include tools for tracking and optimizing energy use, cooling, and environmental impact.

-

Service-based models — Remote monitoring, managed monitoring, analytics-as-a-service will open up access for smaller operators and generate recurring revenue streams.

-

Operational simplicity & integration — Solutions that reduce friction (easy install, good UX, minimal servicing) will earn adoption in a market where downtime risk is high and teams are stretched.

Editorial Perspective

From where I observe, the Data Center Monitoring Market isn’t just about preventing failures — it’s about enabling confident growth. Monitoring becomes a strategic capability: enabling operators to expand capacity, ensure reliability, deliver performance guarantees, and manage sustainability mandates.

Over the next decade, as data centers deploy more edge sites, hybrid models, and as AI workloads press infrastructure limits, visibility will be non-negotiable. Vendors that deliver monitoring that is reliable, intelligent, scalable, and efficient will be the foundation stones of data center operations.