The global automotive pinion gear market is witnessing steady growth, driven by innovation, rising vehicle production, and evolving drivetrain technologies. The market, valued at US$ 11.08 billion in 2023, is forecasted to reach US$ 17.2 billion by 2033, expanding at a CAGR of 4.5 % over the next decade. This upward trajectory reflects increasing demand for high-performance, durable, and lightweight gear systems across automotive applications.

Market Scope: Bevel Gears and Helical Gears in Automotive Systems

A key area of analysis in the automotive pinion gear market is the segmentation by gear type and application. Bevel gears and helical gears are the dominant categories used across critical automotive systems, including steering systems, transmissions, and differentials. Each gear type fulfills specific performance requirements within these systems.

Helical gears are preferred for their smooth operation, efficiency, and ability to handle higher loads, making them ideal for modern steering systems and transmissions. Bevel gears, on the other hand, are widely used in differential systems, where torque must be transmitted at changing angles. This segmentation provides valuable insight into the functional diversity and technological requirements of pinion gears across vehicle components.

Growth Drivers and Market Challenges

The primary driver of market growth is the steady increase in global vehicle production, particularly in developing regions where automotive manufacturing is expanding rapidly. Advances in material science and manufacturing technologies—such as precision machining and advanced heat treatment—are enhancing the durability, efficiency, and cost-effectiveness of pinion gears. The push toward lightweight vehicle components is also spurring the adoption of aluminum and composite materials for gears, which reduce vehicle weight and improve fuel efficiency.

Another growth factor is the use of digital design and simulation tools that optimize gear geometry and performance. These innovations contribute to longer product lifespans, reduced noise, and improved energy efficiency in drivetrains.

However, the market faces notable challenges. The rise of electric vehicles (EVs) is reshaping drivetrain design, potentially reducing the number of traditional mechanical components like pinion gears. EV architectures often employ integrated e-axles or direct drive systems, which differ from conventional gear-based powertrains. Furthermore, gear manufacturers face intense cost pressures, as automotive OEMs demand higher performance at lower production costs. Meeting stringent quality and reliability standards also remains a challenge, particularly for smaller manufacturers seeking to enter the market.

Regional Landscape and Market Dynamics

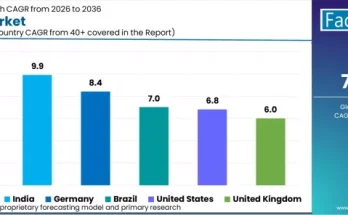

Asia-Pacific dominates the global automotive pinion gear market due to strong automotive production bases in China, India, Japan, and South Korea. Rapid industrialization, growing vehicle ownership, and government incentives for local manufacturing continue to boost demand in this region.

In North America and Europe, the market is characterized by advanced engineering capabilities and high R&D investment. Manufacturers in these regions are focusing on innovation, material improvement, and compliance with emission and safety regulations. Additionally, the robust automotive aftermarket in these regions provides a consistent source of demand for replacement gears.

Other regions, such as Latin America and the Middle East, are experiencing gradual growth, driven by infrastructure expansion and increased demand for commercial vehicles.

Recent Developments and Competitive Landscape

The competitive landscape of the automotive pinion gear market is evolving through mergers, acquisitions, and strategic partnerships aimed at enhancing product portfolios and manufacturing capabilities. Dana Incorporated strengthened its market position by acquiring Oerlikon’s Drive Systems division, expanding its precision gear offerings for light and commercial vehicles. ZF has introduced advanced gearboxes equipped with condition monitoring features to improve predictive maintenance capabilities.

Meanwhile, companies such as Humbel are focusing on gear technologies that align with the electrification trend, developing prototypes suited for e-drives and electric axles. These advancements underscore a shift toward integrating traditional mechanical gear expertise with emerging electric and hybrid powertrain technologies.

The market remains highly fragmented, with both global and regional players competing on innovation, material quality, and cost efficiency. Prominent companies include B&R Machine and Gear Corporation, Bharat Gears Ltd., Eaton Corporation PLC, Gear Motions, Mahindra Gears & Transmissions Pvt. Ltd., Precipart Corporation, Renold PLC, and Samgong Gear Ind. Co. Ltd. Competition centers on precision manufacturing, advanced materials, and long-term partnerships with automotive OEMs.

Segment Insights: Bevel vs. Helical Gear Trends

Helical pinion gears are gaining prominence due to their ability to deliver quiet, efficient power transmission with high load-carrying capacity. These gears are widely used in steering and transmission systems, where performance and smoothness are critical. Bevel gears, however, continue to dominate differential applications, particularly in heavy-duty and off-road vehicles that require high torque transfer and directional changes.

As automotive design continues to evolve, the demand for high-precision, low-noise gears is rising, especially in passenger vehicles. Manufacturers are investing in technologies that enhance performance while maintaining compactness and weight efficiency.