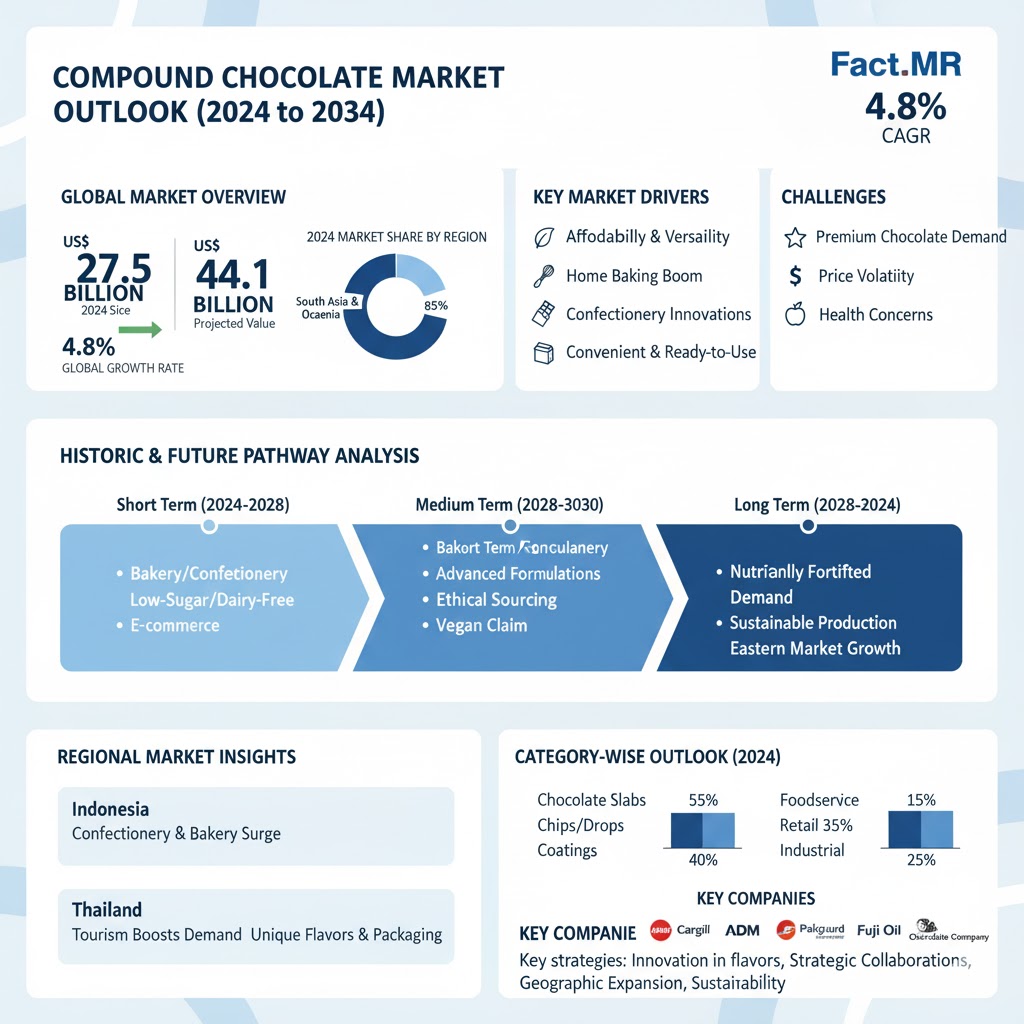

The global compound chocolate market is set to experience robust growth as manufacturers, bakeries, and confectionery brands increasingly turn to cost-efficient chocolate alternatives that deliver premium taste and texture. According to a recent report by Fact.MR, the market is estimated at US$ 27.5 billion in 2024 and is forecasted to expand at a CAGR of 4.8%, reaching approximately US$ 44.1 billion by 2034.

The rising adoption of compound chocolate across bakery, confectionery, and frozen dessert applications—coupled with product innovations emphasizing clean-label, sustainable, and palm-oil-free formulations—is fueling global demand. Manufacturers are enhancing product versatility by offering a wide variety of cocoa, milk, and white chocolate profiles suitable for coating, molding, enrobing, and decorating.

Strategic Market Drivers

Rising Popularity of Cost-Effective Chocolate Alternatives

Compound chocolate serves as a cost-effective substitute for pure chocolate, replacing cocoa butter with vegetable fats while maintaining a desirable taste and mouthfeel. This affordability, coupled with stable melting properties, makes it ideal for large-scale bakery and confectionery applications. As inflationary pressures impact cocoa prices globally, compound chocolate’s economic advantage continues to attract food manufacturers and chocolatiers.

Innovation in Texture, Flavor, and Functionality

Advancements in formulation technology have allowed compound chocolates to closely replicate the flavor, aroma, and texture of real chocolate. Producers are leveraging high-quality cocoa liquor and specialty fats to enhance gloss, snap, and heat stability. Modern variants now feature improved tempering-free properties, superior shelf life, and better performance in tropical climates—key factors driving adoption across Asia and Latin America.

Growing Demand from Bakery, Confectionery, and Dairy Industries

The expansion of artisanal bakeries, café chains, and premium dessert brands has accelerated the use of compound chocolate as a versatile coating and filling material. It is increasingly being used in chocolate bars, cookies, donuts, pastries, ice creams, and coatings due to its ease of handling and consistent results. The rapid rise of the global bakery sector, particularly in emerging economies, provides strong momentum for market expansion.

Sustainability and Ethical Sourcing Initiatives

Consumers’ growing interest in sustainability is prompting producers to shift toward responsibly sourced cocoa and palm-oil alternatives. Industry leaders are investing in transparent supply chains, sustainable sourcing certifications, and eco-friendly packaging solutions to align with ESG goals and global food safety standards.

Regional Growth Highlights

Asia Pacific: The Fastest-Growing Market

Asia Pacific dominates the global compound chocolate landscape, driven by rising confectionery consumption, urbanization, and the expansion of local bakery industries.

In 2022, Barry Callebaut Group announced the groundbreaking of its third manufacturing facility in India, located in Ghiloth Industrial Area, Neemrana, approximately 120 km southwest of Delhi. Upon completion, this facility will make India Barry Callebaut’s largest chocolate-producing market in the Asia Pacific region, with total investments exceeding CHF 50 million over five years.

Meanwhile, Cargill continues to innovate for the Indian market. In 2024, the company introduced its NatureFresh Professional Chocolate Indulgence Range, developed through in-depth research with Indian bakers. This range—featuring Intense Dark, Dark, Milk, and White variants—utilizes Cargill’s proprietary DoMiReCo processing technology to deliver consistent cocoa flavor, creamy texture, and superior color and sheen. Available in slabs and chips, these products offer a 12–15 month shelf life, ideal for bakery and ice cream applications.

Europe: A Hub of Premiumization and Clean Label Trends

Europe’s compound chocolate market is characterized by consumer preference for ethically sourced ingredients and palm-oil-free products. Premium chocolate brands are focusing on clean-label and allergen-free formulations. Western Europe remains the epicenter of chocolate innovation, with countries like Belgium, France, and Germany leading product diversification efforts.

North America: Demand for Custom Formulations Rising

In North America, compound chocolate is witnessing increasing demand from industrial bakers, confectioners, and dairy product manufacturers seeking cost-effective yet high-quality alternatives. The U.S. market is driven by product customization, flavor innovation, and the growing appeal of artisanal and functional chocolate offerings.

Latin America and the Middle East: Emerging Sweet Spots

Emerging markets in Latin America and the Middle East are offering new growth avenues due to evolving consumer preferences and the expansion of local confectionery manufacturing. With supportive trade policies and improved cold chain logistics, these regions are expected to see heightened adoption of compound chocolate in both domestic and export markets.

Challenges and Market Considerations

Despite positive growth trends, the compound chocolate market faces several challenges:

- Volatile Cocoa Prices: Fluctuating raw material costs can impact profit margins.

- Health-Conscious Consumer Shift: Growing demand for low-sugar and natural ingredient formulations necessitates reformulation efforts.

- Competition from Real Chocolate: Rising premiumization in some markets may limit compound chocolate’s appeal in high-end segments.

- Regulatory Compliance: Meeting food safety, labeling, and ingredient disclosure standards across regions requires operational agility.

Competitive Landscape

The global compound chocolate market is moderately consolidated, with major players focusing on innovation, capacity expansion, and strategic partnerships with confectionery and bakery manufacturers.

Key Companies Profiled:

Barry Callebaut; Cargill; ADM; Palsgaard; Fuji Oil; Blommer Chocolate Company; Bellcolade; Puratos; Yake China Co.; Beryl’s Chocolate & Confectionery; Benns; and Other Key Players.

These companies are investing in advanced fat systems, flavor engineering, and localized production facilities to cater to diverse regional taste profiles. Collaborations with artisanal chocolatiers, bakery chains, and industrial confectioners are expected to strengthen their global market positioning.

Conclusion

The compound chocolate market is entering a dynamic growth phase, fueled by affordability, technological innovation, and evolving consumer tastes. As manufacturers prioritize sustainable sourcing and product differentiation, the industry is well-positioned to cater to both mass-market and premium segments—bridging the gap between indulgence and innovation.