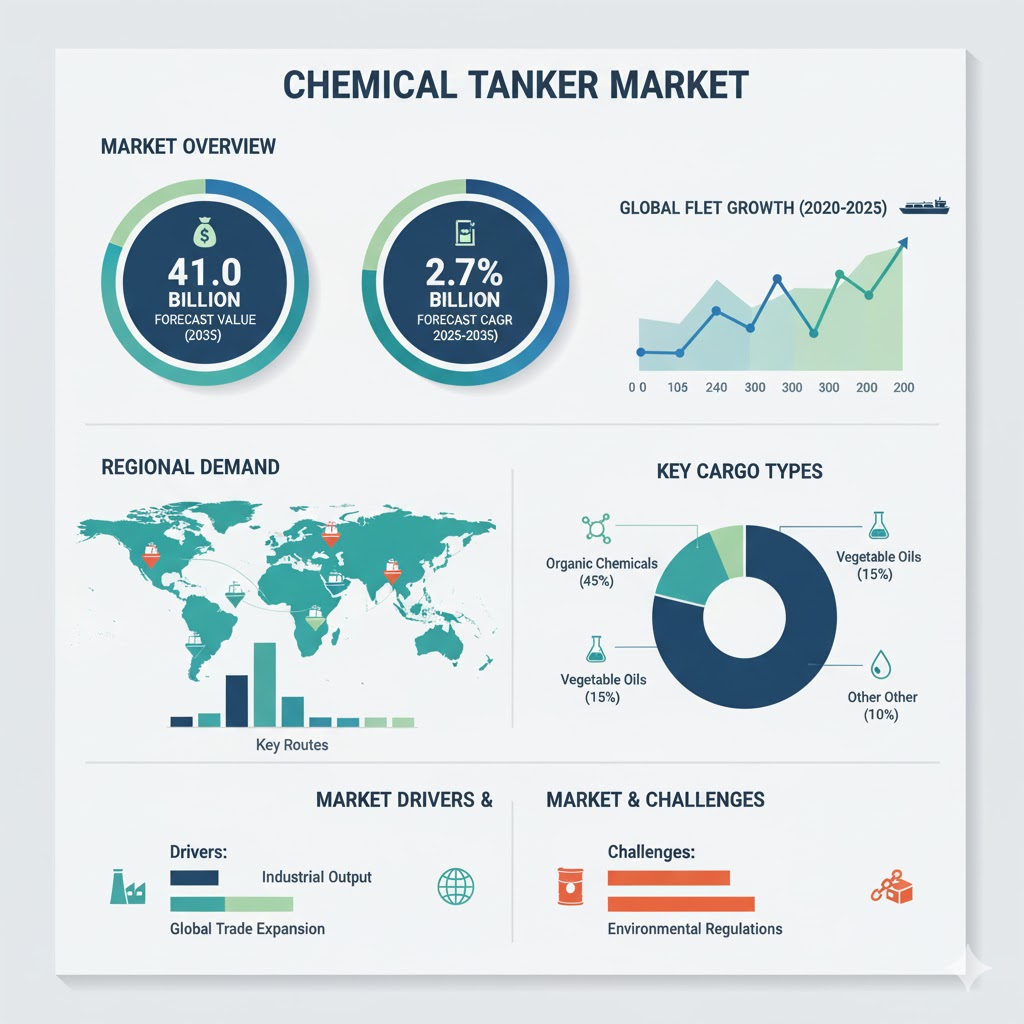

The global chemical tanker market stands at the threshold of a decade-long expansion trajectory that promises to reshape maritime transportation technology and chemical logistics solutions. According to a recent report by Fact.MR, the market is projected to grow from USD 31.5 billion in 2025 to USD 41.0 billion by 2035, reflecting a CAGR of 2.7% over the forecast period.

This steady growth is driven by the rising global trade of chemicals, increasing demand for specialized transport vessels, and stricter international safety and environmental regulations. As the global chemical industry expands and diversifies, the need for dedicated shipping infrastructure—capable of handling hazardous, high-purity, and temperature-sensitive liquids is becoming increasingly critical.

Strategic Market Drivers

- Rising Global Chemical Trade

The accelerating production and export of industrial chemicals, petrochemicals, and specialty products are directly fueling demand for advanced tanker fleets. As emerging economies strengthen their chemical manufacturing bases, long-distance trade routes are witnessing increased tanker deployment. The shift from regional to global supply chains is creating significant opportunities for shipping operators and vessel manufacturers.

- Stricter Environmental and Safety Regulations

Regulatory bodies such as the International Maritime Organization (IMO) are tightening standards on emissions, waste management, and cargo safety. Compliance with the IMO’s MARPOL and IBC Code frameworks has prompted fleet modernization and retrofitting of older vessels. Operators are now adopting double-hulled designs, efficient cargo heating systems, and eco-friendly propulsion technologies to minimize environmental impact and improve operational reliability.

- Technological Advancements in Vessel Design

The introduction of advanced materials, corrosion-resistant coatings, and smart cargo monitoring systems is transforming the performance and durability of chemical tankers. Digitalization and IoT-enabled sensors allow real-time data tracking, ensuring optimal cargo integrity and safety. Furthermore, innovations in fuel efficiency—such as LNG-powered tankers and hybrid propulsion—are enhancing sustainability in marine transport.

- Growth in Specialty and Bio-based Chemicals

The global transition toward bio-based and specialty chemicals has increased the need for segregated and coated tanks capable of handling diverse cargo types. These high-value chemicals demand stringent transport conditions, expanding the market for Type 2 and Type 3 chemical tankers. This shift underscores the industry’s move toward value-added, niche logistics solutions.

Regional Growth Highlights

East Asia: The Maritime Powerhouse

East Asia remains the cornerstone of the chemical tanker market, led by China, Japan, and South Korea. The region’s dominance stems from its vast chemical production capacity, established shipbuilding industry, and strong export networks. Continued investments in maritime infrastructure and eco-friendly ship technologies are expected to reinforce East Asia’s leadership in the coming decade.

Europe: Regulation-driven Growth

Europe’s chemical tanker market is expanding steadily under the influence of strict environmental mandates and a strong chemical manufacturing base in Germany, the Netherlands, and France. European operators are early adopters of LNG-fueled tankers and digital fleet management solutions, aligning with the EU’s decarbonization goals and the “Fit for 55” framework.

North America: Strengthening Trade and Fleet Modernization

The U.S. and Canada are witnessing growing chemical exports, particularly from the petrochemical and shale gas sectors. This trend is driving investments in modern tanker fleets and advanced terminal facilities. The emphasis on safety, energy efficiency, and cross-border trade is expected to sustain North America’s upward market trajectory.

Middle East and Latin America: Emerging Frontiers

Rising chemical production in the Middle East and Latin America is propelling regional demand for chemical tankers. Gulf countries are focusing on diversifying export portfolios beyond crude oil, while Brazil and Mexico are witnessing growth in downstream chemical industries. These regions represent untapped opportunities for new shipping routes and fleet expansions.

Market Segmentation Insights

By Product Type

- Organic Chemicals: Account for the largest market share due to their extensive use in manufacturing plastics, solvents, and fertilizers.

- Inorganic Chemicals: Witness stable demand driven by applications in mining, metallurgy, and water treatment.

- Vegetable Oils and Fats: Represent a growing segment as global trade in edible oils and bio-based products expands.

By Tank Type

- Stainless Steel Tankers: Dominate the market due to superior resistance to corrosion and suitability for a wide range of chemicals.

- Coated Tankers: Gaining momentum for cost-effective transport of less reactive chemicals and bio-based materials.

By Fleet Size

- Small and Medium Tankers: Primarily serve regional and coastal routes, benefiting from flexibility and cost efficiency.

- Large Tankers: Drive international trade, catering to long-haul chemical transport with advanced safety and capacity features.

Challenges and Market Considerations

Despite steady growth, the chemical tanker market faces several key challenges:

- Volatility in Chemical Demand: Economic fluctuations and geopolitical tensions can impact global trade volumes.

- High Capital and Maintenance Costs: Modern vessels require significant investment, especially for eco-friendly retrofits.

- Stringent Safety Regulations: Compliance with international standards increases operational costs but remains non-negotiable.

- Port and Infrastructure Limitations: Developing regions often lack specialized docking and cargo handling facilities, affecting route efficiency.

Competitive Landscape

The global chemical tanker market is characterized by high competition, strategic fleet expansions, and technological collaborations. Key players are focusing on sustainability, digitalization, and performance optimization to enhance global competitiveness.

Key Players in the Chemical Tanker Market:

- Stolt-Nielsen Limited

- Odfjell SE

- MOL Chemical Tankers Pte. Ltd.

- Mitsui O.S.K. Lines, Ltd.

- Scorpio Tankers Inc.

- Nippon Yusen Kabushiki Kaisha (NYK Line)

- Hafnia Limited

- Navig8 Group Pte. Ltd.

- Kawasaki Kisen Kaisha, Ltd. (K Line)

- Eaglestar Marine Holdings (L) Pte. Ltd.

- PerkinElmer

These companies are emphasizing operational efficiency, sustainable shipping, and smart fleet management to maintain a competitive edge. Collaborative ventures with chemical manufacturers and port authorities are also shaping the industry’s strategic roadmap.

Future Outlook: Steering Toward a Smarter, Sustainable Maritime Future

The coming decade marks a transformative phase for the global chemical tanker market. As maritime transport evolves to meet environmental and digital imperatives, the sector is set to witness the rise of eco-efficient vessels, intelligent fleet systems, and AI-driven logistics management.

Manufacturers and shipping operators that integrate sustainability, automation, and compliance into their operations will lead the next wave of innovation in maritime chemical transport. With robust demand fundamentals and continued infrastructure investment, the chemical tanker industry is well-positioned to navigate the tides of change and achieve stable, long-term growth.