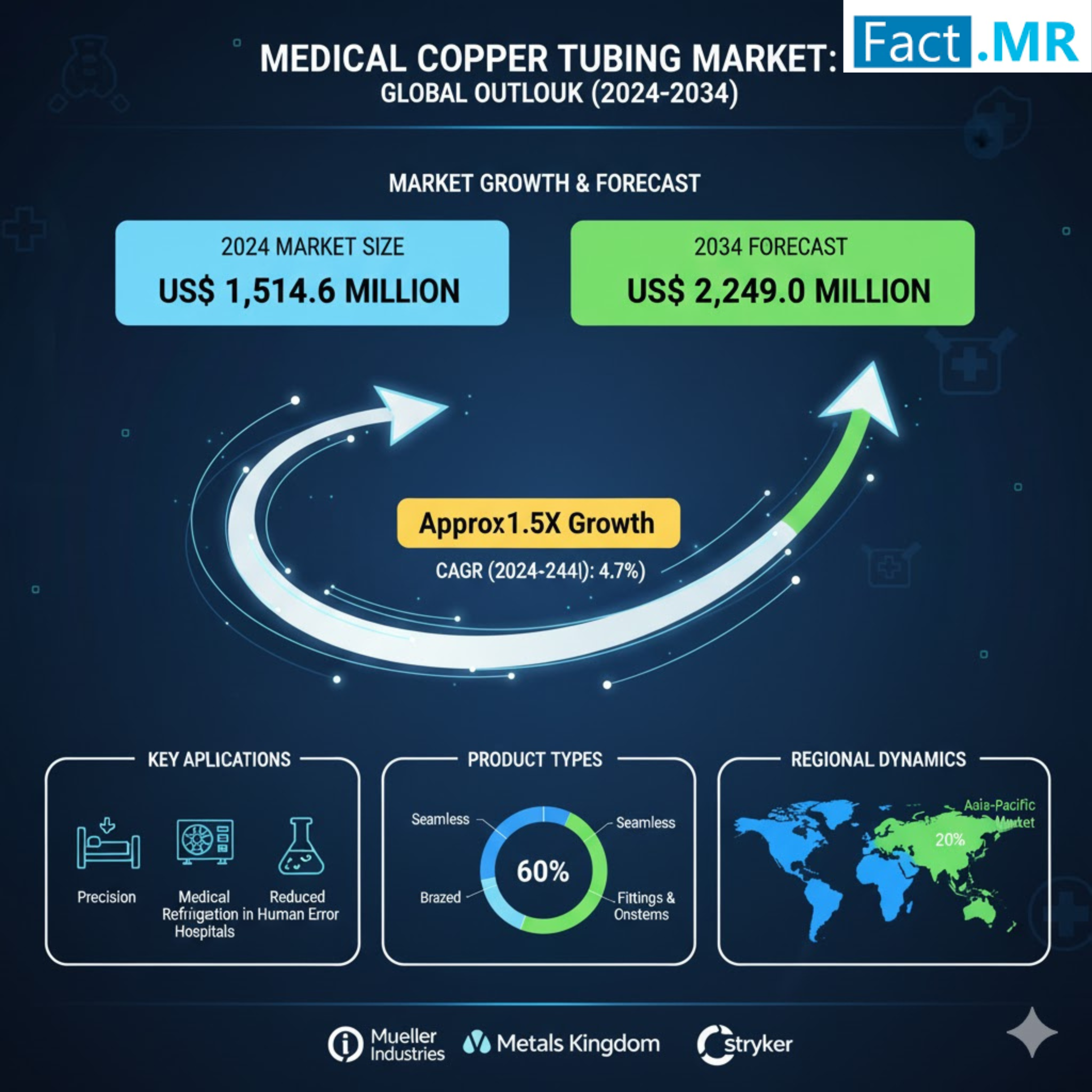

The global Medical Copper Tubing Market is projected to exhibit steady growth through 2034, driven by increasing healthcare infrastructure development, rising demand for medical gases and tubing systems, and enhanced focus on infection control. According to the latest FACT.MR report Medical Copper Tubing Market Trends & Growth Analysis by 2034, the medical copper tubing market size is estimated at USD 1,514.6 million in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 4.0%, reaching USD 2,247.2 million by 2034.

Key Growth Drivers

Several factors are underpinning the rise of medical copper tubing demand globally. A major driver is the expansion of hospitals, clinics, and specialty medical centers around the world, particularly in Asia-Pacific and other emerging regions. As investments increase in medical infrastructure, the need for reliable, durable tubing for medical gases (oxygen, medical air, etc.), diagnostic equipment, and patient care delivery becomes more critical.

Copper tubing is favored for its antimicrobial properties, corrosion resistance, durability, and minimal maintenance needs, all of which are especially important in medical settings. Healthcare facilities increasingly emphasize materials that reduce infection risk and permit sterilization, and copper tubing meets many of these requirements. The trend of miniaturization in medical devices also increases the need for high-quality copper tubes able to perform well in compact and precise configurations.

Governmental regulations and standards that mandate high purity, low friction, and reliable performance in medical tubes are also pushing the adoption of copper tubing in more medical applications. Additionally, eCommerce channels are beginning to play a more prominent role in distribution, expanding access and speeding delivery timelines.

Market Segmentation & Regional Trends

In product segmentation, the tubing segment dominates, accounting for over 98% of the market share in 2024, as copper tubing is core to medical gas delivery, diagnostic devices, and fluid handling in healthcare. Among end-users, hospitals represent the largest share—over 80%—given their continuous need for medical gas systems, operating theaters, ICU/CCU gas supply, and other continuous care services.

Regionally, East Asia stands out as the fastest growing market with a projected CAGR of about 4.9% through 2034. China holds a commanding share in East Asia, contributing significantly to both production and consumption, owing to its large healthcare sector and investments in medical infrastructure. In 2024, China’s medical copper tubing market was valued around USD 347 million, with expectations of significant growth through 2034.

North America maintains a solid share as well, with a lower but steady growth (CAGR ~3.3%) driven by stringent regulatory standards, hospital upgrades, and high standards for infection control. The United States is a key market in this region both in terms of demand for medical copper tubing and adherence to quality and regulatory norms.

Challenges and Restraints

Despite promising growth, the market faces several restraints. Cost is one significant challenge: copper is inherently more expensive compared to alternative materials such as plastics or stainless steel. During periods of high raw copper price volatility, procurement costs can fluctuate considerably, impacting pricing and decision making for hospitals and clinics, especially in budget-constrained or public health sectors.

Another major restraint is the availability of substitutes. Plastic tubing and stainless steel tubing, when properly treated, provide lower cost or greater flexibility in certain applications, and in cost-sensitive regions, these may be preferred. Also, ensuring regulatory compliance, standardization (e.g. purity, pressure ratings, antimicrobial surface treatment), and consistency in quality across producers is nontrivial.

Operational factors, such as installation, maintenance, welding/fitting of tubing systems, and compatibility with existing infrastructure, also affect adoption velocity. Healthcare facilities often weigh upfront costs, total life cycle cost, durability, maintenance requirements, and potential for infection control benefits when selecting tubing materials.

Recent Developments & Trends

Several recent developments are shaping market dynamics for medical copper tubing. In early 2023, Lawton Tubes showcased 100% recyclable medical-grade copper tubes at a major medical convention, reinforcing sustainability and environmental credentials as differentiators.

Also in 2023, the Indian state of Gujarat entered into an agreement with Malaysian copper tube manufacturer Mettube Copper India Private Limited to establish a local manufacturing facility, signifying regional capacity expansion and efforts to localize supply chains.

Another innovation comes from the Wieland Group, which introduced “Cuprolife,” a copper tube composed entirely of recycled copper, emphasizing reduced environmental impact without compromising performance. The group is also investing in copper recycling facilities in Kentucky, USA.

These developments underscore evolving customer demand for sustainability, traceability, and eco-friendly production alongside traditional performance metrics like durability and sterility.

Key Players & Competitive Insights

The medical copper tubing market includes both long-standing and emerging players that are investing in quality, compliance, and innovation. According to recent market reports, major companies profiled include Mueller Industries, Inc.; OmegaFlex Inc.; Cambridge-Lee Industries LLC; Lawton Tube Co. Ltd.; Beacon Medaes; UACJ Corporation; Mandev Tubes; Jiangyin Hehong Precision Technology Co., Ltd.

Other notable names appearing in competitive analyses include KME Group; Wieland Group; ABC Tube Company Pvt. Ltd.; B. Braun SE; Becton, Dickinson and Company; Cerro Flow Products LLC among others. Many of these firms are focusing on material quality (medical-grade copper, antimicrobial surfaces), achieving or maintaining regulatory certifications, enhancing manufacturing technology, and increasing sustainability efforts through recycling and efficient production methods.

Some competition is based on cost leadership, while others are differentiating on value—such as antimicrobial copper, precision tubing for medical gas delivery, zero-leak fittings and bracketing, or bespoke fitting solutions adapted to specialty clinics and ambulatory surgical centers. Supply chain reliability, certification (ASTM, CSA, etc.), and global distribution capability are important competitive levers.

Outlook & Strategic Implications

With the medical copper tubing market expected to grow from USD ~1.51 billion in 2024 to USD ~2.25+ billion by 2034, stakeholders—manufacturers, healthcare providers, distributors, and investors—are advised to take several strategic steps. Manufacturers should prioritize sustainable and recycled copper production, develop tubing solutions with antimicrobial properties, and work on high-precision fittings and accessories that meet stringent regulatory standards.

Healthcare facility planners and hospital administrations should assess the total lifecycle cost of tubing systems, including maintenance, infection risk reduction, and durability benefits of copper over alternatives. Regulatory bodies and governments have a role in harmonizing standards, encouraging use of antimicrobial materials, and incentivizing eco-friendly production.

Emerging markets, especially in Asia-Pacific, offer strong growth opportunity; local manufacturing, partnerships, and capacity expansions are likely to unlock cost advantages and reduce lead times. Additionally, innovations in copper tubes for minimally invasive medical devices and diagnostic equipment miniaturization will further expand the addressable market.

Browse Full Report: https://www.factmr.com/report/medical-copper-tubing-market