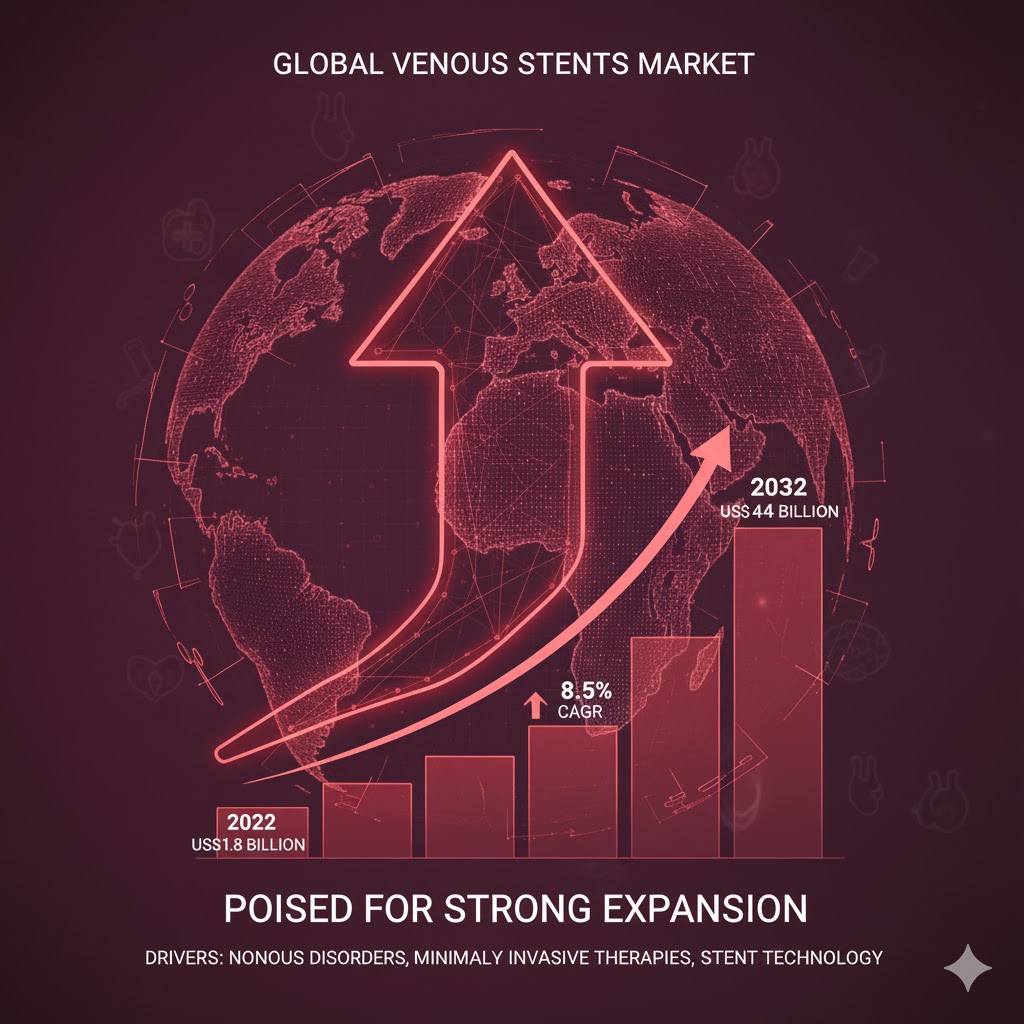

The global venous stents market, currently valued at approximately US$ 1.08 billion (2022), is projected to grow to US$ 2.44 billion by 2032, according to new market intelligence from Fact.MR. This expansion reflects a CAGR of 8.5%, driven by increasing incidence of venous disorders, growing demand for minimally invasive therapies, and advancements in stent technology.

Key Drivers: Growing Venous Disease Burden & Minimally Invasive Treatments

-

Rising chronic venous conditions: Chronic deep vein thrombosis (DVT), post‑thrombotic syndrome (PTS), and May-Thurner syndrome are increasingly diagnosed, boosting demand for venous stents to restore blood flow in obstructed veins.

-

Ageing population: As populations age, the prevalence of venous insufficiency and vascular disorders rises, fueling growth in interventions that leverage stents.

-

Preference for minimally invasive procedures: Physicians are favoring endovascular stenting over open surgical procedures, citing benefits like reduced recovery time, lower complication rates, and less patient discomfort.

-

Technological innovation: Players in the market are investing in flexible self-expanding stents, drug-coated designs, and newer materials like nitinol to improve deployment, patency, and patient outcomes.

Segmentation & Technology Trends

-

Stent Technologies: The market is broadly segmented into iliac vein stent technologies and Wallstent technologies. Wallstents, designed for more flexible, high-stress venous environments, are expected to grow faster, with a projected 9% CAGR over the next decade.

-

Disease Indications:

-

Chronic DVT remains the largest driver, used to treat deep‑vein occlusions especially in the legs.

-

Post-thrombotic syndrome and other vein-related conditions also form a significant share, especially in recurrent or complicated cases.

-

-

Application by Anatomical Site: The most common application remains leg vein interventions, but stents are also frequently used in abdominal, chest, and arm veins as part of broader vascular therapies.

Geographic Trends: Where the Growth Comes From

-

China: The fastest‑growing national market, expected to post a double‑digit CAGR, driven by rising healthcare infrastructure and increased awareness of venous disease.

-

Japan & Europe: Also significant markets, with steady growth supported by older populations, advanced healthcare systems, and strong adoption of interventional vascular therapies.

-

North America: Maintains a strong presence, with a high share of market revenues, as hospitals and specialty vascular centers adopt state‑of‑the‑art stent technologies.

Competitive Landscape

Major companies are pushing innovation and geographical expansion to compete in this high-growth space. Key players include:

-

Becton, Dickinson & Company

-

Boston Scientific Corporation

-

Cook Medical, LLC

-

Gore Medical

-

Jotec GmbH

-

OptiMed Medizinische Instrumente GmbH

These firms are enhancing their portfolios with self-expanding nitinol stents, more deliverable systems, and specialized stents for different venous anatomies.

Challenges & Market Risks

-

High procedure costs: Deploying venous stents requires specialized interventional expertise and imaging, making initial cost high for many healthcare settings.

-

Regulatory & reimbursement issues: In several regions, reimbursement for venous stenting can be complicated or limited, slowing adoption in lower‑coverage markets.

-

Clinical training gap: Optimum placement and long-term outcomes depend on skilled clinicians; lack of experience in venous‑specific stenting may restrain market growth.

-

Device durability & restenosis: Long-term patency is critical; stents must resist restenosis and mechanical fatigue over time, especially in high-mobility venous sites.

Browse Full Report : https://www.factmr.com/report/venous-stents-market

Strategic Outlook & Opportunities

-

Healthcare providers should invest in training vascular specialists and interventional teams to expand venous stenting capacity, particularly in regions with under‑served venous disease populations.

-

Manufacturers can accelerate R&D in drug‑eluting and biodegradable stents, improve stent flexibility, and develop delivery systems tailored for venous anatomy.

-

Policymakers & payers should consider supporting reimbursement frameworks that encourage use of minimally invasive venous therapies, which may ultimately reduce long-term healthcare burden associated with chronic venous disease.

-

Investors looking at high-growth medical device segments should explore companies focused on next-gen venous stents, particularly those developing for emerging markets and novel material systems.