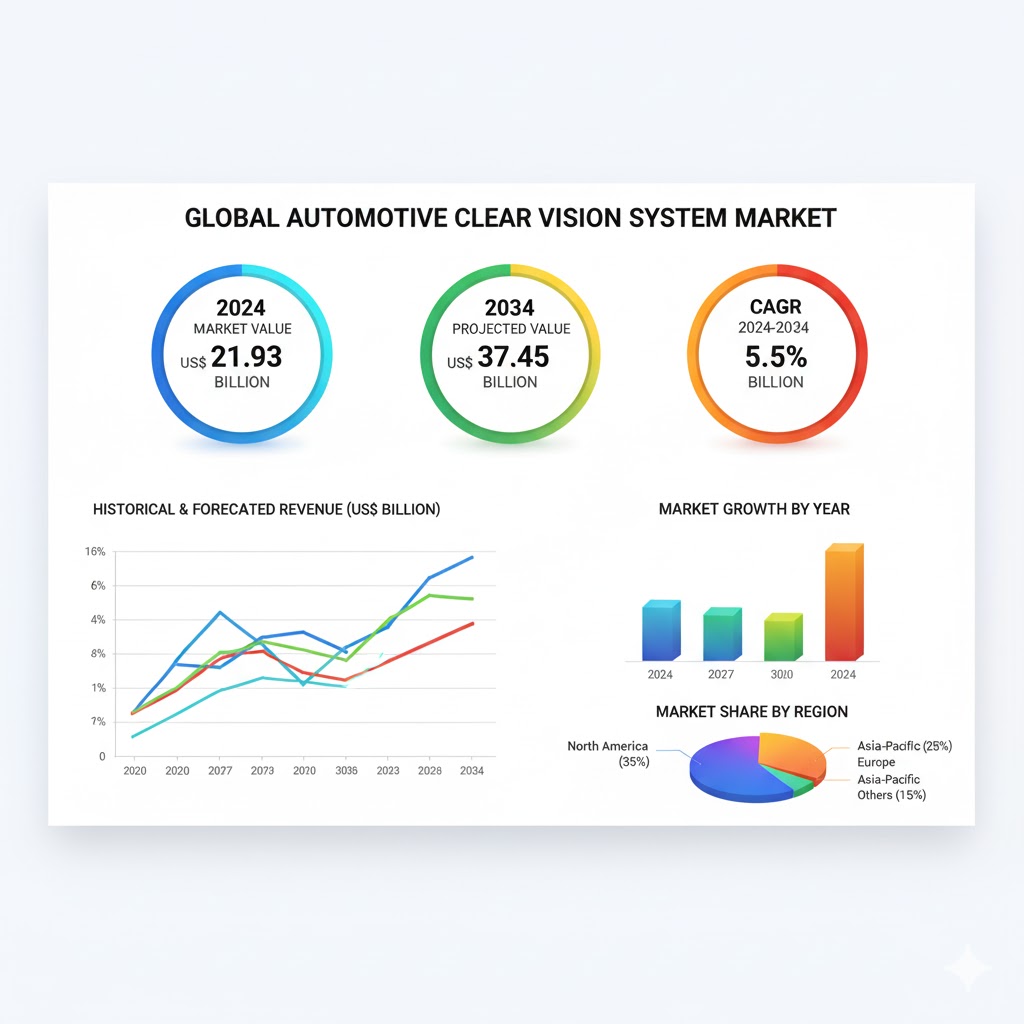

The global automotive clear vision systems market is on track for substantial expansion over the next decade, rising from US$ 21.93 billion in 2024 to US$ 37.45 billion by 2034. This reflects a CAGR of 5.5%, fueled by rising vehicle safety standards, rapid adoption of Advanced Driver Assistance Systems (ADAS), and an increasing need for reliable cleaning solutions that maintain visibility and sensor performance in all driving conditions.

Clear vision systems — including washer fluid reservoirs, pumps, delivery modules, wipers, spray mechanisms, and surface-cleaning technologies — have become essential in modern vehicles. As automotive intelligence advances, keeping both windshields and exterior sensors clean is critical for safety and regulatory compliance.

Why Clear Vision Systems Are Becoming Essential

Safety & All-Weather Visibility

Rapidly changing weather, dust, mud, snow, and road debris can impair driver visibility. Clear vision systems ensure that windshields, cameras, and sensor surfaces remain unobstructed, supporting safer driving conditions and reducing accident risks.

ADAS & Autonomous Vehicle Growth

Modern vehicles rely heavily on cameras, lidar units, radar sensors, and other optical components. These systems must remain clean to ensure precise object detection, lane guidance, and collision avoidance. As more vehicles integrate ADAS and semi-autonomous functionality, demand for sensor-cleaning systems is increasing sharply.

Regulatory Pressure & Consumer Expectations

Governments worldwide continue to strengthen safety regulations, requiring vehicles to maintain proper visibility standards. Meanwhile, vehicle buyers are increasingly prioritizing features that enhance safety, performance, and convenience.

Market Segmentation & Growth Trends

The automotive clear vision systems market is segmented by offering, vehicle type, and distribution channel. Each segment contributes uniquely to the industry’s growth outlook.

Offering-Based Insights

-

Washer Fluid Fill & Storage Systems

This segment is projected to represent nearly two-thirds of the market by 2034. These systems store and deliver cleaning fluids to windshields, headlights, and cameras, ensuring consistent visibility. -

Washer Fluid Management Systems

These advanced systems regulate cleaning fluid usage based on environmental conditions, speed, and sensor contamination, helping improve efficiency and reduce waste. -

Surface Cleaning Systems

Encompassing wipers, sprayers, and mechanical cleaning modules, these systems are critical for ensuring visibility across various vehicle surfaces, including headlights, windshields, and ADAS sensors.

Vehicle-Type Insights

-

Passenger Cars

Passenger vehicles remain the largest market segment. By 2034, they are expected to contribute more than US$ 26 billion in revenue as safety features increasingly become standard — even in mass-market vehicles. -

Commercial Vehicles

Fleets, trucks, buses, and logistics companies rely heavily on visibility and sensor stability for safety and operational efficiency, making this segment an expanding opportunity area.

Distribution Channel Insights

-

OEM (Original Equipment Manufacturers)

The majority of clear vision systems are installed during vehicle production, particularly as automakers embed ADAS and autonomous functionality directly into new models. -

Aftermarket

The aftermarket segment is growing steadily due to fleet upgrades, component replacements, and retrofits for ADAS-enabled vehicles.

Regional Highlights

East Asia Dominance

East Asia currently leads the global market, supported by high vehicle production rates, rapid adoption of ADAS, and strong integration of smart safety technologies. Its market share is projected to expand further by 2034.

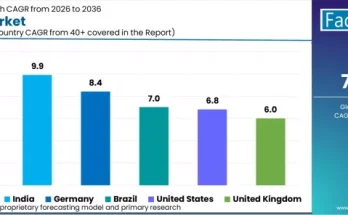

North America Growth

North America is set for healthy expansion driven by increased adoption of premium vehicles, rising interest in intelligent safety features, and strong consumer demand for driver-assistance technologies. The United States, in particular, is expected to generate nearly US$ 5 billion in revenue by 2034.

China’s Strong Momentum

China’s clear vision systems market continues to grow rapidly as domestic automakers adopt advanced technologies and expand EV and ADAS-equipped vehicle production.

Japan’s High-Tech Advantage

Japan’s market is projected to grow significantly over the forecast period, supported by strong engineering capabilities and high consumer adoption of technologically advanced vehicles.

Challenges & Market Constraints

Despite robust growth potential, several challenges could affect market development:

-

Higher System Costs

Clear vision systems incorporate multiple components — including pumps, reservoirs, sensors, and control modules — raising production and maintenance costs. -

Complex Integration Requirements

Sensor-cleaning systems require precise alignment and compatibility with ADAS technologies. Poor integration can compromise sensor performance or cause system malfunctions. -

Aftermarket Adoption Barriers

Retrofitting advanced clear vision systems into older vehicle models can be difficult due to compatibility and design limitations.

Competitive Landscape

The market features a mix of global automotive suppliers and specialized systems manufacturers. Leading companies include:

-

Bosch

-

Continental

-

Valeo

-

Denso

-

HELLA

-

Kautex Textron

-

Trico Products

-

Mitsuba

-

Ficosa

-

Mergon

-

ABC Group

-

Hanwha Systems

-

FLIR Systems (specializing in thermal and night-vision cleaning solutions)

These companies are investing in innovations such as sensor-targeted cleaning, intelligent pump controls, low-power systems for electric vehicles, and modular cleaning units that support next-generation autonomous driving requirements.

Future Outlook & Emerging Innovations

The next decade is expected to bring major advancements in automotive clear vision systems:

-

Integrated Sensor Cleaning

Cleaning modules that automatically clear cameras, lidar, and radar sensors will become standard in autonomous-capable vehicles. -

Smart Fluid Management

Intelligent systems will optimize fluid usage using real-time environmental and sensor data. -

Lightweight, EV-Optimized Designs

As electric vehicles expand globally, vision systems will adopt lighter materials and low-consumption pumps to preserve battery range. -

Growth in Fleets & Aftermarket Upgrades

Commercial fleet operators are increasingly prioritizing visibility technologies to reduce accidents and minimize downtime. -

Rise of Modular Cleaning Platforms

Future systems may feature interchangeable cleaning modules designed to meet the specific needs of various ADAS components.

Quote from Lead Analyst

“Clear vision systems are emerging as critical safety components in both conventional and autonomous vehicles. The projected growth to US$ 37.45 billion underscores how rapidly automakers and fleet operators are investing in technology that keeps vision and sensor functionality reliable under all conditions.”

Browse Full Report : https://www.factmr.com/report/4015/automotive-clear-vision-systems-market

About the Report

This comprehensive study analyzes the global automotive clear vision systems market across offerings, vehicle types, distribution channels, and regions, providing forecasts, competitive intelligence, and trend mapping through 2034.