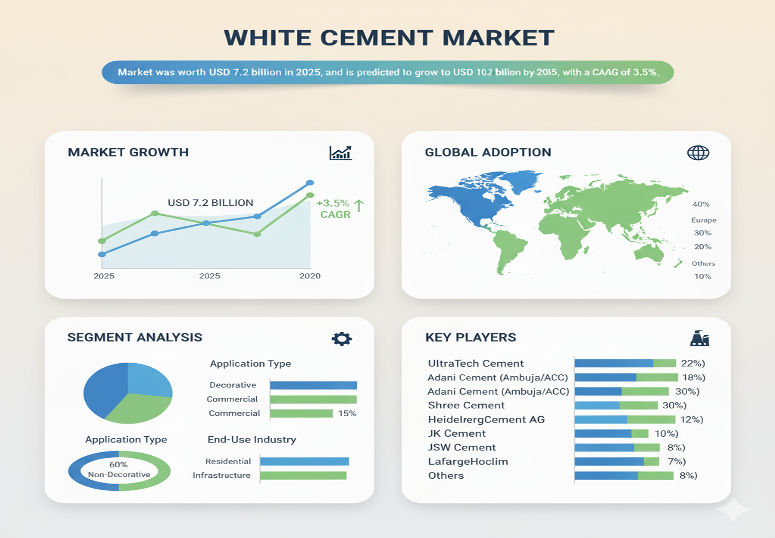

The global white cement market is projected to grow from approximately USD 7.2 billion in 2025 to about USD 10.2 billion by 2035, representing a compound annual growth rate (CAGR) of around 3.5% over the decade. This growth reflects increasing demand from construction and architectural applications where aesthetic finish, whiteness, reflectivity, and premium quality are highly valued. White cement is increasingly specified for decorative finishes, façade applications, architectural precast works and high-quality concrete elements in both residential and commercial projects.

Market Drivers & Demand Catalysts

Several factors are fueling the expansion of the the white cement market. Rapid urbanization and infrastructure development are driving new construction in many regions, leading contractors, concrete producers, and developers to choose white cement for its superior whiteness, ability to accept pigments, and suitability for visible architectural surfaces. White cement offers design flexibility and can help create premium finishes — smooth surfaces, lighter colours, polished concrete, and decorative or ornamental structures. It also reflects heat due to lighter colour, which helps in some climates to reduce thermal absorption in exposed concrete surfaces or roofing panels.

Additionally, increasing interest in sustainable construction practices supports demand, as white cement can complement high-reflectivity building materials aimed at reducing heat island effects and lowering cooling loads in buildings. In interior spaces, white concrete and rendered surfaces with white cement help achieve lighter, brighter environments, reducing need for artificial lighting. Decorative concrete and architectural precast segments increasingly specify white cement to achieve refined finishes in plazas, institutional buildings, hotels, and high-end residential projects.

Product Segmentation & Applications

White cement is offered in several product types including white Portland cement, masonry or blended white cement, and specialty formulations for high early strength or architectural precast applications. Among these, white Portland cement remains the dominant product type due to its strength, consistency, colour purity, and broad applicability in precast decorative concrete, architectural elements, or load-bearing concrete that also demands aesthetic appearance.

In terms of application, the construction segment is dominant. This includes residential construction (exteriors, interior floors, decorative finishes), commercial construction (façades, hotels, retail centers, offices) and infrastructure projects incorporating decorative or visible concrete elements. Precast concrete products, architectural panels, ornamental elements, terrazzo floors, mouldings, decorative overlays, and façade claddings are common applications that benefit from the whiteness and consistency of white cement. Mortars, tile adhesives, grouts and repair mortars also represent significant demand, especially where matching white or light finishes is important in renovation or restoration work.

Regional Insights & Growth Potential

Regionally, growth is uneven but promising across both mature and emerging markets. In regions with stringent building aesthetics standards and premium architectural projects, adoption of white cement is strong. Emerging economies are catching up: rapid urbanization, rising incomes, and demand for high-quality infrastructure and architectural projects are driving demand in Asia, the Middle East, Latin America and Africa.

Some mature markets continue to adopt white cement in refurbishments, restoration works, and high-end constructions. Meanwhile, regions with hot climates benefit from the reflective properties of white cement in reducing heat absorption in exposed concrete elements or roofing surfaces. In emerging economies, developers are increasingly using white cement in residential high-end projects, decorative precast elements and architectural finishes to enhance visual appeal and quality.

Competitive Landscape & Strategic Trends

The white cement market is populated by cement manufacturers, suppliers of specialty cement blends, precast concrete producers, and architectural concrete specialists. Competitive players differentiate by purity of whiteness, consistency, early strength, pigment compatibility, value-added specialty blends, and regional production capacities. Many producers are investing in production technology improvements, kiln controls, raw material purity (low iron content), and chemical formulation to reduce discolouration or grey tints, ensuring high whiteness and uniform shade.

Manufacturers often expand regional production or set up dedicated lines for white cement to meet demand for architectural and decorative construction. Partnerships with architectural firms, precast manufacturers, and interior design contractors allow producers to specify white cement as part of turnkey decorative or high-finish concrete packages. Some also offer special colour formulation with admixtures or pigments to provide customized aesthetic finishes.

Challenges & Market Restraints

Despite positive growth, there are some constraints. The cost of producing white cement is higher than grey or ordinary cement because raw materials must have low iron and other impurities, and manufacturing processes are more exacting to maintain whiteness. This pushes up the product cost, which may limit adoption especially in cost-sensitive or lower-income markets. Installation and casting with white cement often require more control over aggregates, pigments, mix design, and finishing to maintain the purity of finish, which may increase labor or quality control costs.

In renovation or restoration projects, matching existing finishes or achieving consistency may require more careful material handling. Also, in some regions, regulatory or quality standards may not differentiate white vs grey cement strongly, so buyers may opt for cheaper alternatives unless aesthetic or functional benefits are mandated.

Forecast & Strategic Recommendations

Looking ahead to 2035, the white cement market is expected to grow steadily from USD 7.2 billion in 2025 to USD 10.2 billion, reflecting a solid growth trajectory at a 3.5% CAGR. Companies should focus on optimizing manufacturing for lower cost and higher purity, establishing regional production to reduce shipping costs, and introducing specialty blends tailored for decorative, precast, or high early strength applications.

Marketing efforts should highlight the aesthetic advantages, pigment compatibility, and reflective / thermal benefits in hot climate regions. Partnerships with architectural and precast concrete firms will help specify white cement for high-visibility projects. Offering product formulations for specific climate conditions or architectural finishes can be a differentiator, especially in high value markets.

Browse Full Report: https://www.factmr.com/report/white-cement-market

Editorial Perspective

White cement occupies a unique niche in construction materials: combining structural performance with aesthetic purity. As architecture trends toward more visible, high-finish concrete surfaces and developers focus on premium finishes, white cement becomes more than a material — it becomes part of the signature look of buildings and design elements. Companies that deliver high whiteness, consistent quality, regional availability, and cost efficiency will be well positioned to ride the steady growth to 2035 in this differentiated construction materials segment.