The global aircraft engines market is set to experience robust expansion, projected to rise from USD 78.2 billion in 2025 to USD 183.4 billion by 2035, registering a CAGR of 8.9%, according to the latest market outlook. Driven by the surging demand for fuel-efficient aircraft, the rapid recovery of commercial air travel, and technological advances in sustainable propulsion, the market is entering an era of accelerated transformation.

Aviation’s shift toward sustainability has become the most defining force in the aircraft engine market. Engine manufacturers are rapidly transitioning from conventional jet engines to hybrid-electric and open-fan propulsion systems designed to lower emissions, reduce fuel burn, and meet stringent environmental regulations.

The introduction of next-generation geared turbofan (GTF) and open rotor designs has elevated performance standards across the aviation industry. These engines deliver higher thrust efficiency while minimizing noise, making them the go-to solution for airlines seeking to reduce operational costs and environmental footprints.

Governments and regulatory bodies, particularly in North America and Europe, are offering significant funding and incentives to encourage zero-emission aviation technologies. Collaborations between aerospace leaders and energy innovators are accelerating R&D in hydrogen-fueled and hybrid-electric engines, signaling a turning point in the journey toward decarbonized flight.

The growth trajectory of the aircraft engines market is closely tied to the global resurgence in air travel and the expansion of commercial fleets. Rising urbanization, middle-class growth, and tourism recovery are driving airlines to modernize and expand their fleets with more fuel-efficient and quieter aircraft.

Commercial aviation remains the dominant end-use sector, accounting for the majority of global engine demand. Fleet modernization and rising deliveries of narrow-body aircraft are contributing to higher turbofan adoption, particularly in emerging markets across Asia-Pacific and Latin America.

Meanwhile, business and general aviation is witnessing record growth, spurred by the post-pandemic preference for private and charter flights. Manufacturers are increasingly focusing on lightweight, efficient turboprop and hybrid-electric engines to serve this growing segment, which aligns with evolving customer preferences for on-demand mobility and sustainable operations.

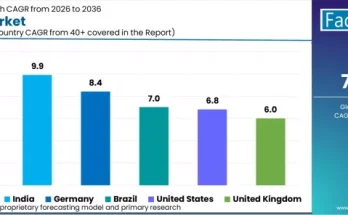

Asia-Pacific continues to dominate the global market, fueled by rapid fleet expansion in China, India, and Southeast Asia. Local aircraft programs, such as COMAC’s C919, are propelling the development of indigenous propulsion technologies. China’s “Made in China 2025” initiative and heavy government investment in aerospace innovation have positioned the region as a hub for next-generation engine manufacturing.

North America remains a key market, anchored by aerospace giants GE Aerospace, Pratt & Whitney, and Honeywell. These players lead in R&D, focusing on hybrid-electric and open-fan propulsion systems. The U.S. market, supported by strong defense aviation demand and sustainability-focused policies, continues to set the global benchmark in performance and innovation.

Europe, driven by leaders like Rolls-Royce and Safran, is leveraging the EU Green Deal and Horizon Europe funding frameworks to pioneer clean propulsion solutions. The region’s strong emphasis on sustainability and defense investment—particularly in France, Germany, and the U.K.—is boosting market resilience and innovation.

Emerging aviation hubs in the Middle East and Africa are also witnessing steady growth. Fleet modernization efforts in the UAE and Saudi Arabia, along with Africa’s growing focus on regional air connectivity, are expected to strengthen regional demand through 2035.

Technological Segmentation: Where the Growth Lies

- By Engine Type:

Turbofan engines continue to lead due to their proven efficiency and adaptability across short- and long-haul fleets. However, electric and hybrid-electric engines are poised to be the fastest-growing category as aviation enters the era of decarbonization. - By Technology:

Conventional engines remain the backbone of current aviation fleets. In contrast, hybrid and open rotor engines are gaining traction, integrating innovative designs that reduce fuel consumption by up to 30% and support the use of Sustainable Aviation Fuels (SAFs). - By End-Use:

Commercial aviation dominates the market, but business aviation is emerging as a high-growth opportunity, particularly for manufacturers developing efficient, lightweight propulsion systems for smaller aircraft and electric vertical take-off and landing (eVTOL) models.

Challenges on the Horizon

Despite the promising outlook, the aircraft engines market faces challenges. High R&D and certification costs create barriers for new entrants, while stringent emission and noise regulations add layers of complexity to production cycles. Additionally, supply chain constraints—particularly for turbine components and electronics—continue to impact delivery timelines and profit margins.

Moreover, as manufacturers simultaneously invest in conventional and next-generation propulsion, balancing production capacity and technological development remains a strategic challenge. However, these hurdles are driving innovation, encouraging new collaborations, digital integration, and predictive maintenance systems to enhance engine reliability and efficiency.

Competitive Landscape: Innovation Takes Flight

The global market is dominated by industry heavyweights such as GE Aerospace, Pratt & Whitney, Rolls-Royce, and Safran, which collectively shape the evolution of modern propulsion. These firms are leveraging partnerships, mergers, and acquisitions to strengthen their foothold in sustainable aviation technologies.

For instance:

- GE Aerospace’s RISE Program (2024) introduced an open-fan engine architecture targeting 20% improved fuel efficiency and hybrid-electric readiness.

- Pratt & Whitney’s GTF Advantage Initiative (2024) focuses on enhancing geared turbofan durability and performance for narrow-body aircraft.

Emerging competitors from China (AECC), Japan (IHI Corporation), and India (HAL) are entering the global market with indigenous innovations and regional partnerships, intensifying global competition.

Opportunities for Industry Leaders

The aircraft engine industry stands at a pivotal juncture where sustainability, digitalization, and performance converge. As demand for fuel-efficient and low-emission engines accelerates, the next decade will reward manufacturers that can deliver modular, lightweight, and SAF-compatible propulsion systems.

The push toward hybrid-electric and hydrogen-based engines presents a multi-billion-dollar opportunity for OEMs and suppliers to capture emerging market share. With growing collaboration between aerospace firms, research institutions, and energy providers, the race to define the future of flight is intensifying.

The global aircraft engines market is on course for unprecedented growth, driven by fuel efficiency, sustainability, and innovation. With forecasts indicating an expansion to USD 183.4 billion by 2035, manufacturers that embrace next-generation propulsion and digital integration will define the next era of aviation excellence.

Browse Full Report: https://www.factmr.com/report/2119/aircraft-engines-market