The global automotive soft trim interior market is projected to expand from USD 5,801 million in 2025 to USD 9,722 million by 2035, reflecting a CAGR of 5.3% over the forecast period. This growth is being driven by rising consumer demand for premium comfort, increasing adoption of electric vehicles (EVs), and stringent sustainability regulations pushing automakers toward eco-friendly materials.

Market Overview

Automotive soft trim interiors include seating materials, door panels, dashboards, headliners, and other interior components made from leather, synthetic leather, polymers, and fabrics. The market has seen a shift toward lightweight, durable, and sustainable materials in response to consumer preferences for premium and personalized vehicle interiors, as well as regulatory mandates on carbon emissions and recyclability.

-

Market Size (2020): USD 4,754 million

-

Market Size (2025E): USD 5,801 million

-

Market Size (2035F): USD 9,722 million

-

Historical CAGR (2020–2024): 3.9%

-

Forecast CAGR (2025–2035): 5.3%

Over the next decade, the industry is expected to grow 1.7X, creating an incremental dollar opportunity of USD 3,921 million, reflecting substantial potential for investment and market expansion.

Market Drivers

-

Premium & Personalized Interiors: Increasing consumer preference for comfort, aesthetics, and luxury features is prompting automakers to adopt high-quality materials such as leather, Alcantara, and advanced fabrics.

-

Technological Advancements: Innovations in bio-based composites, smart textiles, self-cleaning fabrics, and AI-driven customization are transforming vehicle interiors, particularly in EVs and autonomous vehicles.

-

Sustainability & Regulatory Compliance: Stricter global regulations are driving the use of eco-friendly materials such as recycled fabrics, plant-based textiles, and biodegradable polymers.

-

EV & Autonomous Vehicle Adoption: Lightweight and durable materials improve battery efficiency, noise insulation, and cabin comfort, aligning with the transition to electric and autonomous mobility.

-

Material Innovation: Development of bio-prepregs, advanced polymers, and smart fabrics presents opportunities for differentiation and premium positioning in the market.

Market Restraints

-

High Production Costs: Premium and sustainable materials often require higher production costs, which can challenge manufacturers in maintaining competitive pricing.

-

Supply Chain Disruptions: Limited availability of raw materials and global supply chain constraints can impact production schedules and market stability.

-

Material Substitution: Traditional materials such as basic fabrics and plastics compete with high-end alternatives, creating pricing and adoption pressures.

Regional Insights

-

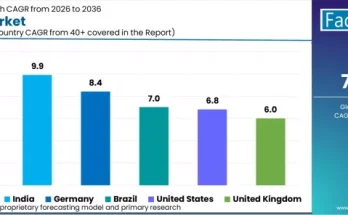

Asia-Pacific: Leading the global market due to rapid urbanization, rising disposable income, and strong automotive production, particularly in China and India. The region is becoming a hub for both production and consumption of advanced soft trim interiors.

-

North America: Strong automotive industry and high luxury vehicle demand, coupled with regulatory support for sustainable materials, support continued growth. The U.S. market is expected to reach USD 2,783 million by 2035 at a CAGR of 4.8%.

-

Europe: Sustainability initiatives and focus on eco-friendly innovation are driving demand for recycled and biodegradable soft trim materials. Germany and France are major design and manufacturing centers for premium interiors.

Country-Specific Outlook

-

United States:

-

Market Value (2025): USD 1,734 million

-

CAGR (2025–2035): 4.8%

-

Market Value (2035): USD 2,783 million

Premium vehicle demand and EV adoption are driving growth. Automakers such as Tesla, Ford, and GM are investing in lightweight, eco-friendly soft trim solutions.

-

-

China:

-

Market Value (2025): USD 1,058 million

-

CAGR (2025–2035): 5.9%

-

Market Value (2035): USD 1,874 million

Rapid urbanization and a growing middle class, combined with government incentives for EVs, are fueling demand for sustainable interiors. Manufacturers like BYD and NIO are investing in synthetic leather and plant-based textiles.

-

-

Japan:

-

Market Value (2025): USD 476 million

-

CAGR (2025–2035): 6.1%

-

Market Value (2035): USD 858 million

Japanese OEMs such as Toyota, Honda, and Nissan focus on high-performance synthetic fabrics, self-cleaning textiles, and AI-enhanced comfort features, driven by EV and hydrogen vehicle initiatives.

-

Segment Analysis

By Vehicle Type:

-

Passenger Vehicles: Dominant segment, including sedans, SUVs, EVs, and hatchbacks. Consumer preference for luxury, comfort, and innovative interior designs drives demand.

-

Light Commercial Vehicles & Heavy Commercial Vehicles: Focused on durability, cost-effectiveness, and functionality, particularly for long-term operational efficiency.

By Material Type:

-

Polymers (PU, PVC, TPEs): Lightweight, cost-effective, and highly customizable. Used for dashboards, door panels, and seating elements.

-

Fabrics: Common in mid-range and economy vehicles. Innovations include antimicrobial, stain-resistant, smart, and temperature-regulating fabrics.

-

Genuine Leather: Premium segment preference for durability, comfort, and aesthetic appeal.

-

Synthetic Leather: Cost-effective alternative for luxury appearance and sustainability goals, increasingly used in EVs.

Technological Trends

-

Smart Interiors: AI and IoT integration, self-cleaning textiles, adaptive surfaces, and ambient lighting.

-

Sustainable Materials: Increased adoption of biodegradable, recycled, and bio-based polymers and fabrics.

-

Advanced Manufacturing: 3D printing and AI-driven supply chain optimization are enhancing production efficiency and customization.

Competitive Landscape

The market is competitive, with top players holding 32–44% market share, while tier II players and others account for the remaining 56–68%. Key companies include:

-

Adient PLC: Leader in seating and soft trim materials; focuses on recycled and bio-based materials.

-

Grupo Antolin Irausa: Roof headliners, door panels, noise-reducing solutions, and sustainable textiles.

-

Benecke-Kaliko AG: Synthetic leather, coated textiles, PU-based breathable materials, and self-repairing surfaces.

-

TS Tech Co.: High-performance seat fabrics, foam cushioning, temperature-sensitive, and self-cleaning fabrics.

-

GST AutoLeather Inc.: Premium natural and synthetic leather for luxury automotive brands.

-

DK Leather Corporation & Mayur Uniquoters Ltd: Specialty in high-end leather and synthetic leather solutions.

-

Magne International Inc.: Lightweight metal-trimmed soft interior components for weight reduction.

Market Outlook (2025–2035)

The automotive soft trim interior market is expected to experience substantial growth, driven by:

-

Increasing consumer demand for luxury, comfort, and personalization.

-

Technological advancements in smart and sustainable materials.

-

Transition to EVs and autonomous vehicles, increasing the need for lightweight, durable, and eco-friendly interiors.

-

Stringent global sustainability mandates and circular economy initiatives.

-

Rapid expansion of emerging automotive markets in Asia-Pacific.

Browse Full Report : https://www.factmr.com/report/479/automotive-soft-trim-interior-market

The market’s future will be defined by the integration of AI-enabled smart interiors, self-sustaining and recyclable materials, and a balance of comfort, durability, and eco-friendliness. Automakers and suppliers investing in innovative, sustainable, and high-quality soft trim materials are best positioned to capture growth in this evolving sector.