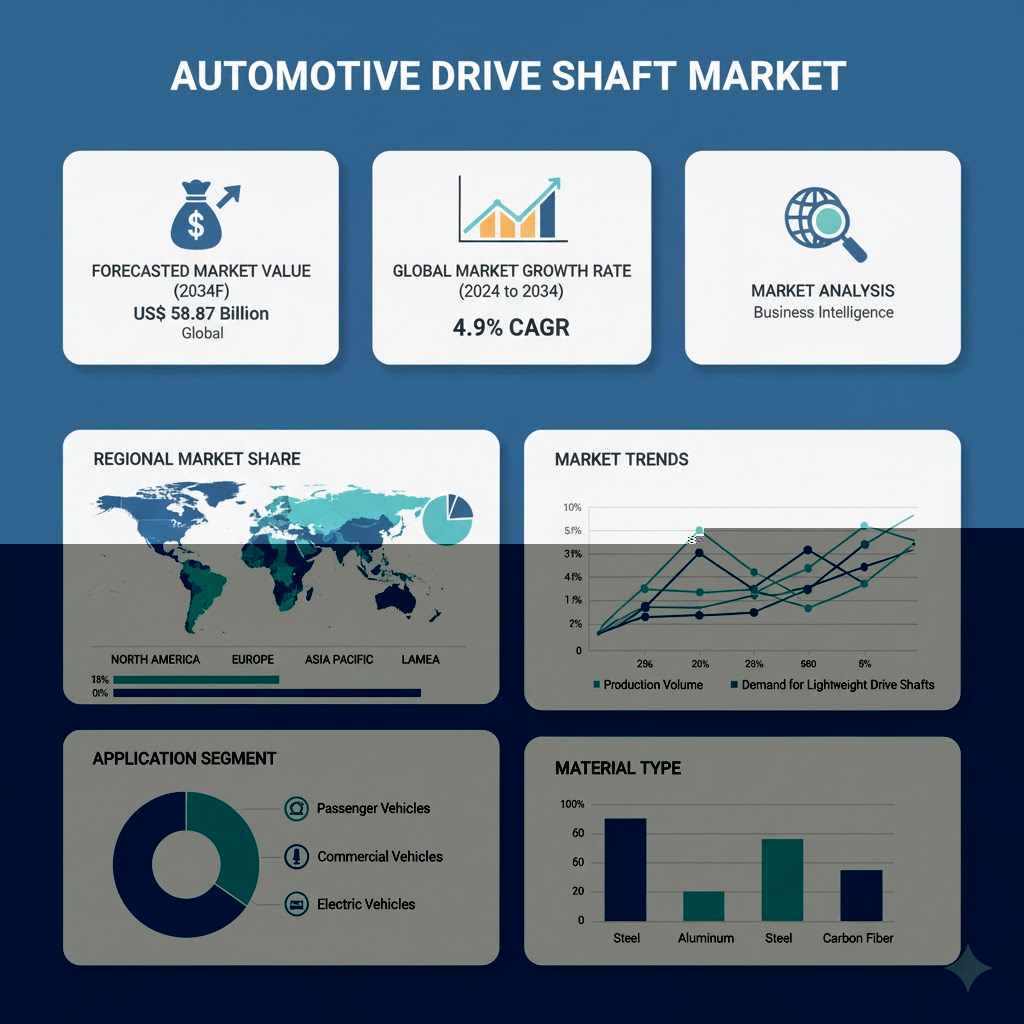

The global automotive drive shaft market is gearing up for a decade of steady expansion, driven by advancements in vehicle design, electrification, and material innovation. According to a newly published report by Fact.MR, the market is estimated at US$ 36.49 billion in 2024 and is projected to reach US$ 58.87 billion by 2034, reflecting a CAGR of 4.9% over the forecast period.

As the automotive industry transitions toward sustainability, safety, and enhanced performance, demand for high-strength, lightweight, and durable drive shafts continues to rise across passenger and commercial vehicle segments.

Strategic Market Drivers

- Electrification and Lightweighting Initiatives

Automotive OEMs are increasingly focusing on fuel efficiency and emission reduction, which has accelerated the adoption of lightweight materials such as carbon fiber and aluminum in drive shaft manufacturing.

Electric vehicle (EV) manufacturers, in particular, demand precision-engineered drive shafts capable of handling high torque and rotational speeds, ensuring smooth power transmission with minimal vibration.

- Expanding Vehicle Production and Aftermarket Demand

The surge in global vehicle production, coupled with growing automotive aftermarket sales, is fueling the need for reliable and high-performance drive shafts. Rapid urbanization, infrastructure expansion, and rising disposable incomes in developing economies further stimulate automotive sales, strengthening market growth.

- Technological Advancements and Integration of Smart Components

Drive shaft manufacturers are integrating advanced technologies such as torque sensors, vibration dampers, and dynamic balancing systems to enhance performance and reliability. Digital monitoring and predictive maintenance solutions are also being introduced to improve vehicle efficiency and minimize downtime.

Regional Growth Highlights

Asia Pacific: The Manufacturing Powerhouse

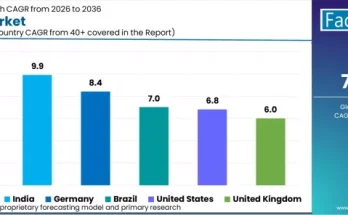

Asia Pacific dominates the global automotive drive shaft market, led by China, Japan, and India. Strong manufacturing ecosystems, expanding automotive production capacities, and the presence of global OEMs contribute to the region’s leadership.

In particular, India’s growing commercial vehicle segment and China’s rapid EV adoption are boosting drive shaft production and export activities.

North America: Focus on Innovation and High-Performance Vehicles

The U.S. and Canada are experiencing growing demand for performance vehicles, SUVs, and EVs. Manufacturers are investing in research and development to produce lightweight, high-strength drive shafts that meet rigorous performance and safety standards.

Europe: Driven by Electrification and Stringent Emission Norms

Europe’s stringent emission policies and strong EV adoption are shaping the regional market. Germany, the U.K., and France are investing in advanced composite materials and energy-efficient technologies to enhance vehicle performance and reduce carbon footprints.

Emerging Markets: Rapid Motorization and Industrial Growth

Latin America, the Middle East, and Africa are witnessing a rise in automotive assembly operations and aftermarket service centers. Increasing government initiatives toward local manufacturing and industrialization are expected to fuel market penetration in these regions.

Market Segmentation Insights

By Type

- Single Piece Drive Shaft: Preferred for light commercial and passenger vehicles due to ease of installation and cost efficiency.

- Two Piece Drive Shaft: Common in heavy vehicles and SUVs for improved load distribution and torque handling.

- Carbon Fiber Drive Shaft: Gaining traction in high-performance and EV segments for weight reduction and enhanced strength.

By Vehicle Type

- Passenger Cars: Largest segment, driven by mass production and rising personal mobility demand.

- Commercial Vehicles: Growing use in logistics, construction, and e-commerce transport fleets.

- Electric Vehicles: Fastest-growing segment due to integration of advanced drivetrain technologies.

Challenges and Market Considerations

- Raw Material Price Fluctuations: Volatile steel, aluminum, and carbon fiber costs impact manufacturing economics.

- EV Drivetrain Complexity: Transition to electric powertrains requires reengineering of shaft design and load dynamics.

- Supply Chain Disruptions: Logistics constraints and geopolitical tensions affect raw material and component availability.

- Competition from Alternative Propulsion Systems: Growing focus on hub motors and direct-drive technologies may limit traditional shaft demand in certain EV models.

Competitive Landscape

The global automotive drive shaft market is moderately consolidated, with leading players emphasizing technological innovation, lightweight materials, and strategic collaborations with OEMs.

Key Companies Profiled:

- GKN Automotive

- Dana Incorporated

- American Axle & Manufacturing Holdings, Inc.

- Nexteer Automotive

- Hyundai Wia Corporation

- NTN Corporation

- Neapco Holdings

- Showa Corporation

- Hitachi Astemo, Ltd.

- IFA Rotorion

These companies are focusing on regional expansion, capacity enhancement, and partnerships to strengthen their market presence and supply chain resilience.

Recent Developments

- March 2023 – Dana Incorporated launched a new series of carbon composite drive shafts designed for EVs, offering 40% weight reduction and enhanced torque capacity.

- November 2022 – GKN Automotive introduced an advanced modular eDrive system integrating high-performance shafts optimized for next-generation electric platforms.

Future Outlook: Driving Toward a Connected and Sustainable Mobility Era

The next decade will mark a transformative phase for the automotive drive shaft industry, shaped by electrification, digital integration, and sustainability. Manufacturers are expected to leverage AI-driven design, advanced composites, and predictive maintenance technologies to deliver smarter, lighter, and more durable solutions.

With the automotive sector rapidly evolving toward zero-emission and high-efficiency mobility, the automotive drive shaft market is poised for sustained growth. Industry leaders that prioritize innovation, material efficiency, and global collaboration will define the future of automotive power transmission.