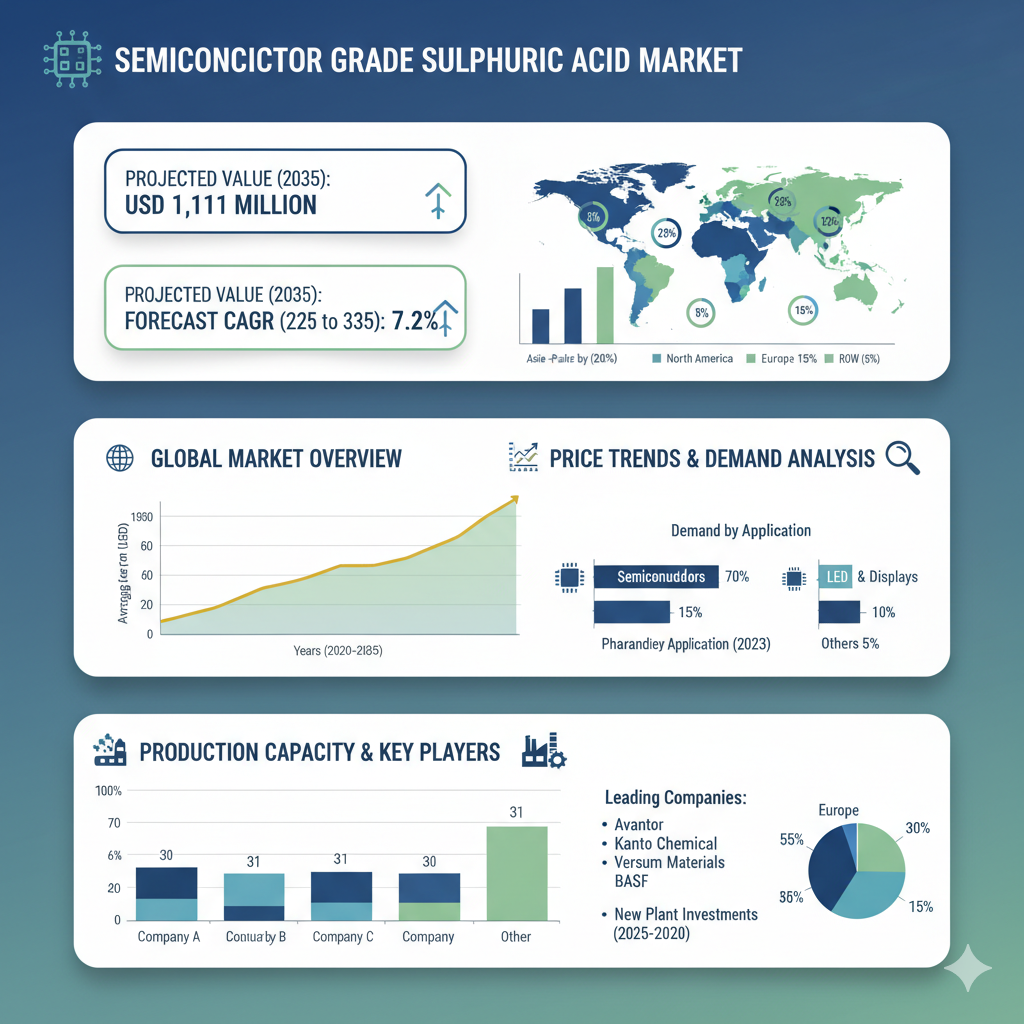

The global semiconductor-grade sulphuric acid market is on a strong uptrend. The market is expected to grow from around USD 554.5 million in 2025 to USD 1,111 million by 2035, expanding at a CAGR of 7.2% over the forecast period.

This robust growth is underpinned by escalating demand for high-purity chemical reagents in semiconductor fabrication, the proliferation of foundries, and the push toward advanced nodes (≤ 7 nm). The shift to EUV lithography, higher cycle counts of wafer cleaning, and investments in domestic semiconductor manufacturing further reinforce this trajectory.

Market Segmentation: Product, Application, End-User, and Region

By Product Characteristics

The market is categorized by purity grade, concentration, and packaging or form. The purity grade includes PPT (parts per trillion, above 99.999%), PPB (parts per billion, 99.99%–99.999%), and Technical Grade (below 99.99%). The PPT-grade segment stands out as essential for critical wafer processing steps and is projected to grow strongly owing to demand from advanced-node fabs.

Standard concentrations such as 96%, 98%, and other special grades like 95%, 97%, and above 98.5% are used depending on process requirements. Delivery modes range from bulk (ISO tanks, tankers, and IBCs) to packaged drums and carboys, as well as specialized containers designed to maintain ultra-high purity during handling and transport. Each of these product attributes plays into procurement decisions by semiconductor fabs, considering handling safety, contamination risk, and supply-chain logistics.

By Application

Key application segments include cleaning processes, etching, texturing, ion implantation, doping, and chemical mechanical planarization (CMP). Cleaning remains the predominant application, where sulphuric acid, often paired with hydrogen peroxide, is used to remove organic residues, photoresists, and contaminants from wafer surfaces.

By End-User

The end-user segmentation includes Integrated Device Manufacturers (IDMs), Pure-play Foundries, OSAT Providers (Assembly and Test), EMS Providers (Electronics Manufacturing Services), and R&D or university laboratories. Foundries and IDMs, with large-scale wafer fabrication operations, constitute the majority of demand, especially for PPT-grade acid in advanced processes. OEMs and EMS units use comparatively smaller volumes but still require certified, high-purity reagents to ensure product consistency and quality.

By Region

Regional segmentation covers North America, Latin America, Europe, East Asia, South Asia, and the Middle East and Africa. East Asia remains a dominant demand hotspot, driven by major semiconductor hubs in China, Taiwan, Korea, and Japan. North America’s growth is supported by governmental initiatives such as the CHIPS Act, which aims to repatriate semiconductor manufacturing. Europe, with its advanced microelectronics capacity in countries like Germany, the Netherlands, and France, is focusing on high-quality and sustainable chemical sourcing.

Growth rates vary across regions. For example, the purity grade segment is projected to grow at nearly 7.9% CAGR, while concentration segments may grow more modestly at around 6.3% over the same period.

Recent Developments & Competitive Landscape

Recent Developments

The semiconductor-grade sulphuric acid market has seen several strategic moves in recent years. In April 2025, BASF announced the construction of a new semiconductor-grade sulphuric acid production facility in Ludwigshafen, Germany. This major investment aims to enhance Europe’s supply chain for ultra-clean chemicals and is expected to be operational by 2027.

In May 2023, Fujifilm acquired the electronic chemicals business from Entegris for USD 700 million, including its high-purity process chemical lines such as sulphuric acid. This acquisition has strengthened Fujifilm’s position in the semiconductor materials sector.

Competitive and Key Players

The semiconductor-grade sulphuric acid market is moderately concentrated, with a handful of key chemical companies holding technological and market leadership. Major players include BASF SE, FUJIFILM Electronic Materials, Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., Stella Chemifa Corporation, KMG Chemicals (Cabot Microelectronics), Avantor Inc., Honeywell International Inc., Showa Denko (Resonac Holdings), Tosoh Corporation, Sachem Inc., DSM Semichem LLC, and Kanto Chemical Co. Ltd.

Competition in this market centers around purity performance, process innovation, and supply reliability. Companies strive to deliver consistent ultra-low metal and ion contamination levels, invest in advanced purification technologies such as distillation and ion exchange, and establish production sites close to major semiconductor fabs to reduce logistics risks. Regulatory compliance and sustainability initiatives are also increasingly shaping market competitiveness.

Request for Discount: https://www.factmr.com/connectus/sample?flag=S&rep_id=10955

Buy Now at USD 4500: https://www.factmr.com/checkout/10955

Check out More Related Studies Published by Fact.MR Research:

Silicon Carbide (Carborundum) Market: https://www.factmr.com/report/4581/silicon-carbide-market

Hydrocarbon Solvents Market: https://www.factmr.com/report/hydrocarbon-solvents-market

Cohesive Automated Equipment Market : https://www.factmr.com/report/cohesive-automated-equipment-market

Anisotropic Conductive Film Market: https://www.factmr.com/report/5315/anisotropic-conductive-film-acf-market