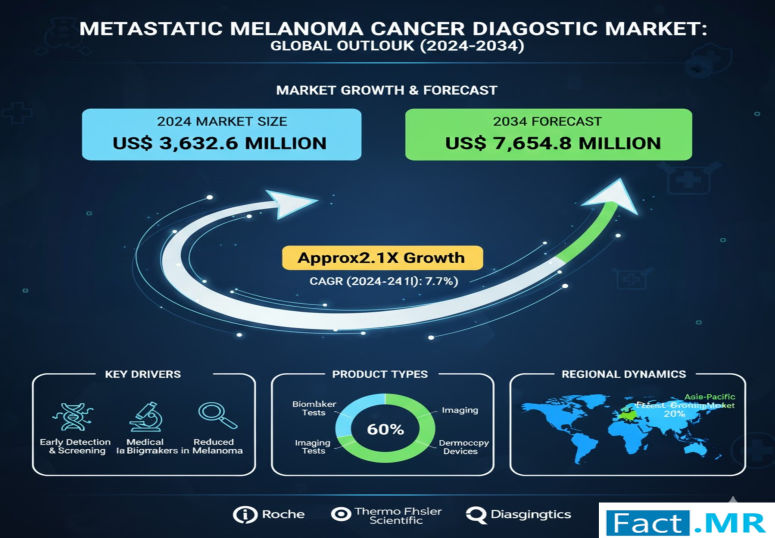

The global metastatic melanoma cancer diagnostic market is set for robust growth in the coming decade, spurred by increasing patient awareness, technological advances, and expanding screening efforts. According to the latest Metastatic Melanoma Cancer Diagnostic Market report by Fact.MR, the market was valued at approximately USD 3,632.6 million in 2024 and is forecast to grow at a compound annual growth rate (CAGR) of 7.70% through 2034, reaching roughly USD 7,601.0 million by 2034.

Request for Discount: https://www.factmr.com/connectus/sample?flag=S&rep_id=9551

Market Dynamics & Growth Drivers

The rise in melanoma incidence, especially metastatic melanoma, is one of the most important factors fueling demand for diagnostic tools. Public awareness campaigns, better screening programs, and early detection emphasize not just identifying melanomas but also catching malignancies before spread. These trends have created growing demand for advanced diagnostic modalities like PET scans, CT, MRI, ultrasound, chest X-ray, and — at the forefront — biopsies for accurate staging and molecular profiling.

Healthcare providers and patients are also increasingly favoring minimally invasive diagnostics, faster turnaround times, and high-sensitivity tests that reduce false negatives. Advances in imaging resolution, biomarker research, and molecular diagnostics are helping clinicians detect melanoma metastasis earlier, guiding treatment planning more effectively. Meanwhile, government programs in the United States, China, India, and other countries are investing in cancer diagnostic infrastructure, boosting adoption of advanced tests.

Segmentation & Regional Insights

By test type, biopsy is a significant contributor to market value, accounting for about 27.0% share in 2024, reflecting its role as a gold standard in diagnosis and staging. Imaging modalities such as PET scans are also growing rapidly, given their ability to detect metastases and assess disease spread.

Regarding end users, pathology laboratories hold a dominant share—around 51.8% in 2024—because they perform the majority of biopsies, molecular tests, and diagnostic analyses, especially in cancer staging and treatment decision-making. Hospitals and cancer research centres follow, but the trend toward outsourcing diagnostics or leveraging specialized labs is pushing growth in pathology services.

Regionally, North America leads the market with about 47.6% share in 2024, underpinned by advanced healthcare infrastructure, high melanoma incidence, and strong investment in diagnostic imaging and molecular testing. The U.S. alone accounts for a large part of this market in North America. East Asia, led by China, shows promising growth with a projected CAGR around 10-10.5% through 2034. China already holds a commanding proportion of East Asia’s market (approximately 76.2% in 2024) due to expanding healthcare access, rising awareness, and capability upgrades.

Recent Developments & Innovation

In recent years, multiple breakthroughs have added impetus to the metastatic melanoma diagnostic market. Early in 2023, a laboratory test known as AMBLor, developed by Avero Diagnostics (licensed from AMLo Biosciences), was introduced to improve early-stage melanoma detection. This reflects growing interest in low-risk, early detection diagnostics that can influence treatment decisions without the invasiveness of full procedures.

Also in 2023, DeepX Diagnostics earned FDA 510(k) clearance for its digital dermatoscope, DermoSight, which leverages image analytics to assist clinicians in identifying skin lesions more accurately. Its use in Europe, and planned entrance into the U.S. market, illustrates the trend of digital imaging tools accelerating diagnostic capacity outside classic pathology labs.

Another notable development is Dermalyser, an AI-driven diagnostic tool demonstrated to reach ~95% sensitivity and 86% specificity in primary care settings. This type of solution offers the potential to triage suspicious lesions earlier, reducing burden on specialists and increasing access to care.

These advancements reflect broader trends in metastatic melanoma diagnostics: integration of AI and image analysis, faster detection methods, teledermatology, digital tools that complement traditional lab-based methods, and newer molecular tests.

Challenges & Restraint Factors

Despite strong projections, several limitations may slow adoption in certain geographies. Diagnostic test cost remains high, especially for advanced imaging (PET, MRI) and molecular profiling, limiting access in low- and middle-income regions. Public awareness, although rising, still has gaps, particularly in resource constrained areas, which inhibit early detection and screening uptake.

Regulatory challenges, reimbursement issues, and infrastructure barriers (availability of pathology labs, imaging equipment, skilled technicians) are other significant inhibitors. False positives/negatives, accessibility to molecular diagnostic tools, and consistency of test quality are concerns especially where lab accreditation is variable. Also, while innovative tools (AI, digital dermatoscopes) are promising, clinician acceptance, validation, and integration into clinical workflows can be slow.

Key Players & Competitive Landscape

Key players in the metastatic melanoma cancer diagnostic market include Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, Abbott Laboratories, QIAGEN, Bristol Myers Squibb, Illumina, Bio-Rad Laboratories, Myriad Genetics, Genomic Health, Agilent Technologies, Exact Sciences, bioMérieux, Hologic, Inc., NanoString Technologies, Guardant Health, Sysmex Corporation, Foundation Medicine, GRAIL, and Menarini Silicon Biosystems.

These companies are focused on developing and refining technologies such as high-resolution imaging, molecular assays, next-gen sequencing panels, liquid biopsy, advanced dermatoscopes, and AI-augmented analysis tools. Some are expanding molecular profiling services to detect genetic mutations associated with melanoma, supporting both diagnostic accuracy and treatment personalization. Others are investing in tools to improve detection in primary care or via telehealth to reach underserved populations.

Increasing partnerships among device/image analytics firms, biotech companies, and hospital systems are accelerating deployment. Regulatory approvals, clinical validations, and product differentiation (sensitivity, specificity, turnaround time, cost) are key competitive levers.

Outlook & Strategic Implications

With the metastatic melanoma diagnostics market expected to more than double in value from 2024 to 2034, reaching approximately USD 7.6 billion, stakeholders across healthcare, diagnostics, government, and technology sectors should prepare for transformational growth.

For diagnostic companies, the opportunity lies in improving accuracy, reducing cost, expanding access, and accelerating regulatory approvals. Innovation in imaging methods, AI, and molecular diagnostics—especially liquid biopsy and non-invasive methods—will be increasingly important. For hospitals and health systems, investing in pathology and imaging infrastructure, training clinicians and technicians, and implementing screening programs earlier in disease progression can improve outcomes and reduce costs.

Public health authorities and governments have an essential role to play: creating awareness campaigns, ensuring reimbursement policies support early detection testing, and supporting regulatory frameworks that incentivize innovation without compromising safety.

Browse Full Report: https://www.factmr.com/report/metastatic-melanoma-cancer-diagnostic-market