Usage-based insurance (UBI)—also known as telematics or pay-how-you-drive (PHYD), pay-as-you-drive (PAYD), and manage-how-you-drive (MHYD)—is transforming auto insurance. Rather than relying on static profiles, premiums are now personalized based on actual driving behavior: miles driven, speed, braking patterns, and more. Insurers embed smart sensors via OBD-II dongles, black boxes, or smartphone apps to track driving data, enabling safer driving rewards and accurate risk assessment

Market Outlook & Growth Drivers

Fact.MR reports the usage insurance market reached approximately US$ 30 billion in 2020, with strong projections to hit US$ 150 billion by 2031, growing at a CAGR of around 17%. This represents a fivefold increase from 2021 to 2031.

Several factors fuel this rapid growth:

- Personalized Pricing– UBI empowers drivers with tailored premiums. PAYD, which accounts for 55% of the market, charges based on actual driving, making insurance fairer.

- Telematics Maturity– Widespread adoption of connected-car tech and smartphones supports UBI implementation globally.

- EV & Safety Awareness– Rising electric vehicle use and road safety focus are boosting telematics investments.

- Cost Optimization– Insurers benefit from better risk modeling, cost control, and service innovation.

- Environmental Advantage– UBI encourages reduced driving, lower emissions, and social benefits.

Policy Types & Technologies

- PAYD: High market share (~55%) encourages safe driving and cost-conscious behavior.

- PHYD/MHYD: Offer deeper behavioral insights using real-time driving analytics.

UBI Tracking Technologies:

- Black Box: Installed behind the dashboard for accurate data logging.

- OBD-II Dongle: Plug-and-play telematics tools.

- Smartphone Apps: Cost-effective and accessible with growing usage.

Smartphone-based solutions are growing at around 9% CAGR due to convenience and lower deployment costs.

Regional Landscape

- North America leads UBI adoption, driven by connected-car penetration. The U.S. accounts for over 50% of global UBI demand.

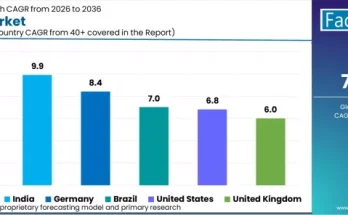

- Europe follows closely with about 10% CAGR—especially robust in Germany, France, the UK—backed by embedded telematics and vehicle safety policies .

- Asia-Pacific is emerging (≈15% CAGR) led by telematics growth in India, China, Japan, and Korea.

- Latin America, MEA, and Eastern Europe are poised for future growth, supported by rising vehicle fleets and digitalization.

Market Potential & Challenges

Opportunities:

- Growing EV Adoption– Ideal synergy with driving analytics.

- Fleet Management– UBI is expanding beyond individual drivers into commercial fleet monitoring.

- Strategic Partnerships– Insurer collaborations with OEMs and telematics providers (e.g., State Farm + Ford, MSIG + AIS) enhance service reach.

- Embedded Telematics– OEM-level hardware pre-installed in vehicles supports OEM-driven insurance models.

Constraints:

- Privacy Concerns– Consumer reluctance due to continuous data tracking.

- Regulatory Variability– Varying laws on data use and driver consent across regions.

- Initial Investment– Technology setup costs for both insurers and policyholders.

Competitive Ecosystem

Major insurers in the UBI landscape include Progressive, Allstate, State Farm, Liberty Mutual, Allianz, AXA, Aviva, Metromile, TrueMotion, Cambridge Mobile Telematics, Octo Group, and Teltonika.

These insurers are:

- Enhancing Telematics– Building in-house data platforms and apps.

- Forging Tech Partnerships– Collaborating with auto manufacturers and IoT startups to scale offerings.

- Launching Pay-As-You-Drive Products– Many are participating in fairness-driven premium models.

Innovation & Use Cases

- Behavioral Feedback– Real-time scoring systems and safe-driving coaching help reduce accidents.

- Smartphone Integration– The rise of app-based UBI solutions attracts tech-savvy millennials.

- Connected Platforms– By Miles and others offer in-car premium tracking.

- Advanced Fleet UBI– Commercial vehicle usage is optimized via UBI-driven cost and safety tools.

- Self-Installed UBI Devices– Lower barrier to use (plug-and-play devices) driving adoption.

Future Outlook

Fact.MR projects the UBI market to reach circa US$ 150 billion by 2031 (17% CAGR). Other analysts estimate growth to over USD 212 billion by 2029 (26% CAGR).

Key drivers forward:

- Automaker Telematics– OEM-integrated UBI systems.

- Regulatory Backing– Policies that support safer, transparent premium models.

- Machine Learning– Enhanced risk prediction via AI.

- Insurance as a Service– Usage-based models toggle into broader mobility solutions.

Conclusion

Usage-based insurance is accelerating the shift from one-size-fits-all to personalized, dynamic vehicle coverage. With telematics, AI, and embedded systems converging, UBI is unlocking value for insurers and drivers alike—offering precision pricing, enhanced safety, and sustainable impact.

Its projected fivefold market expansion by 2031 underscores its transformative effect on insurance and mobility. Stakeholders that navigate technology, privacy, and policy will lead the charge in shaping the next era of personalized, behavior-driven protection.